When considering your home loan application, banks and financial institutions will check your CIBIL score. While there is no specific number regarding the CIBIL score for housing loans, being in a good or excellent score range can certainly make your approval process smooth.

A strong CIBIL score can improve your chances of loan approval and help you negotiate better interest rates and loan terms. Understanding the CIBIL score for home loans and how the score affects your home loan journey is essential to making informed, confident financial decisions.

Read on to know more about the best CIBIL score for home loans and how to improve your score if it is low.

| Although there is no specific number for an ideal CIBIL score, a range of 750 or above is considered best for securing better home loan terms, lower interest rates, and faster loan approval. |

Minimum CIBIL Score for Home Loan

The CIBIL score is a three-digit numerical representation of an individual’s credit usage. It is calculated by various credit bureaus, like TransUnion CIBIL. The CIBIL score ranges between 300 and 900.

Although there is no ideal CIBIL score for a home loan, a score of 750 or above is preferred for the smooth progress of your application. A score in this range is considered a strong indicator of creditworthiness, suggesting that the borrower has a reliable track record of repaying debts on time.

While a score of 750 and above is best, some lenders may consider applications with scores between 700 and 749, though this often comes with stricter terms, such as higher interest rates or lower sanctioned loan amounts. A few non-banking financial companies (NBFCs) might even offer home loans to individuals with scores as low as 600-650 or even 550 (very rarely), but these loans usually involve additional scrutiny and less favourable conditions.

If your CIBIL score falls below 700, it doesn’t necessarily mean your application will be rejected, but lenders may require additional documentation, a co-applicant with a higher score, or a larger down payment to offset the perceived risk.

|

The ideal range of credit score for the best interest rates on your home loan is between 750 and 900. The minimum CIBIL score for a home loan can be as low as 600-650 in almost all cases. However, the loan options will be few, and the repayments or the loan terms can be uneasy. |

Lenders Offering Home Loans & CIBIL Score Range

Different lenders prefer different scores for the straightforward process of a home loan application. It is always best to have a higher score on the CIBIL range. However, in real-life situations, knowing which lender is best to approach for home loans according to your CIBIL score can help you choose wisely.

Following is a rough estimate of top lenders and their preferred CIBIL score range:

Banks Offering Home Loans

| HDFC Bank | 800 and above | 7.90%* Onwards |

| State Bank of India (SBI) | 800 and above | 7.50%* p.a. Onwards |

| ICICI Bank | 750 and above | 8.75%* p.a. Onwards |

| Axis Bank | 751 and above | 8.35%* p.a. Onwards |

| Kotak Mahindra Bank | 800 and above | 7.70%* p.a. Onwards |

NBFCs Offering Home Loans

| LIC Housing Finance | 800 and above | 7.50%* p.a. Onwards |

| Bajaj Finserv | 725 and above | 7.45%* p.a. Onwards |

| Tata Capital | 750 and above | 7.75%* p.a. Onwards |

| PNB Housing Finance | 750 and above | 8.25%* p.a. Onwards |

Please note that the above-mentioned interest rates are only for representative purposes and are subject to change as they are dependent on various factors specific to the borrower.

Suggested Read: Credit Score Range

Top Home Loan Options in India for Low CIBIL Scores

Most banks prefer a higher CIBIL-scored individual under normal circumstances. Still, home loans are not exclusive to high-CIBIL-score owners. But you can get the best interest rates and offers with a higher CIBIL score.

However, there are other options for home loans with low CIBIL scores. There are several NBFCs that provide credit with very interesting terms.

1. Tata Capital Housing Finance

| Minimum CIBIL Score | Around 600 |

| Interest Rate | 7.75%* p.a. Onwards |

Key Features:

- Trusted NBFC with flexible eligibility terms and conditions

- Offers home loans for purchase, construction, and extension

- Accepts lower credit scores with supporting documents (e.g., salary slips, income proof)

- Available for salaried and self-employed applicants

2. Indiabulls Housing Finance

| Minimum CIBIL Score | Around 600 |

| Interest Rate | 8.75%* p.a Onwards |

Key Features:

- A popular lender in India for low to moderate credit score borrowers

- Provides quick online approval and processing

- Focus on property valuation and current repayment capacity

- Accepts informal income documentation, however, for eligible profiles

3. Aditya Birla Housing Finance

| Minimum CIBIL Score | Around 600 |

| Interest Rate | 7.75%* p.a Onwards |

Key Features:

- Accepts mid-to-low CIBIL scores with a stable income history

- Allows balance transfers and top-up loans even with a low credit score

- Offers longer tenure options and competitive EMI plans

- Trusted brand and known for transparent processes

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

4. PNB Housing Finance

| Minimum CIBIL Score | Around 620–650 |

| Interest Rate | 8.25%* p.a. Onwards |

Key Features:

- A recognised housing finance company backed by a public sector bank

- Provides loans to applicants with borderline or recovering credit scores

- Prioritises employment status and asset strength over score alone

- Offers fast-track approvals for salaried applicants

Apart from the lenders themselves, you can also use loan aggregators like BuddyLoan to find the best low-credit score home loans.

5. Buddy Loan (Loan Aggregator)

| Minimum CIBIL Score Supported | Below 650 accepted |

| Role | Aggregator platform, not a direct lender |

Key Features:

- Connects users to multiple Banks and NBFCs offering home loans for poor credit

- Single application matches you with eligible lenders based on your profile

- No hard credit pull is needed at the enquiry stage

- Ideal for comparing offers, interest rates, and eligibility before applying

- Partners may include Tata Capital, Indiabulls, Aditya Birla, and others

Importance of CIBIL Score for Home Loans

Your credit score is a direct indicator of your creditworthiness, credit responsibility, and repayment history. It can be used to evaluate your:

- repayment capacity,

- repayment history,

- credit utilisation,

- existing debts, and

- length of your credit history.

This ultimately aids them in deciding whether to grant the credit amount or not.

For home loans, where the borrowed amount and repayment tenure are typically large, lenders use the CIBIL score as a first-level risk assessment tool; it can be used to understand the past credit usage. A higher score signals that you’re financially disciplined and more likely to repay the loan on time.

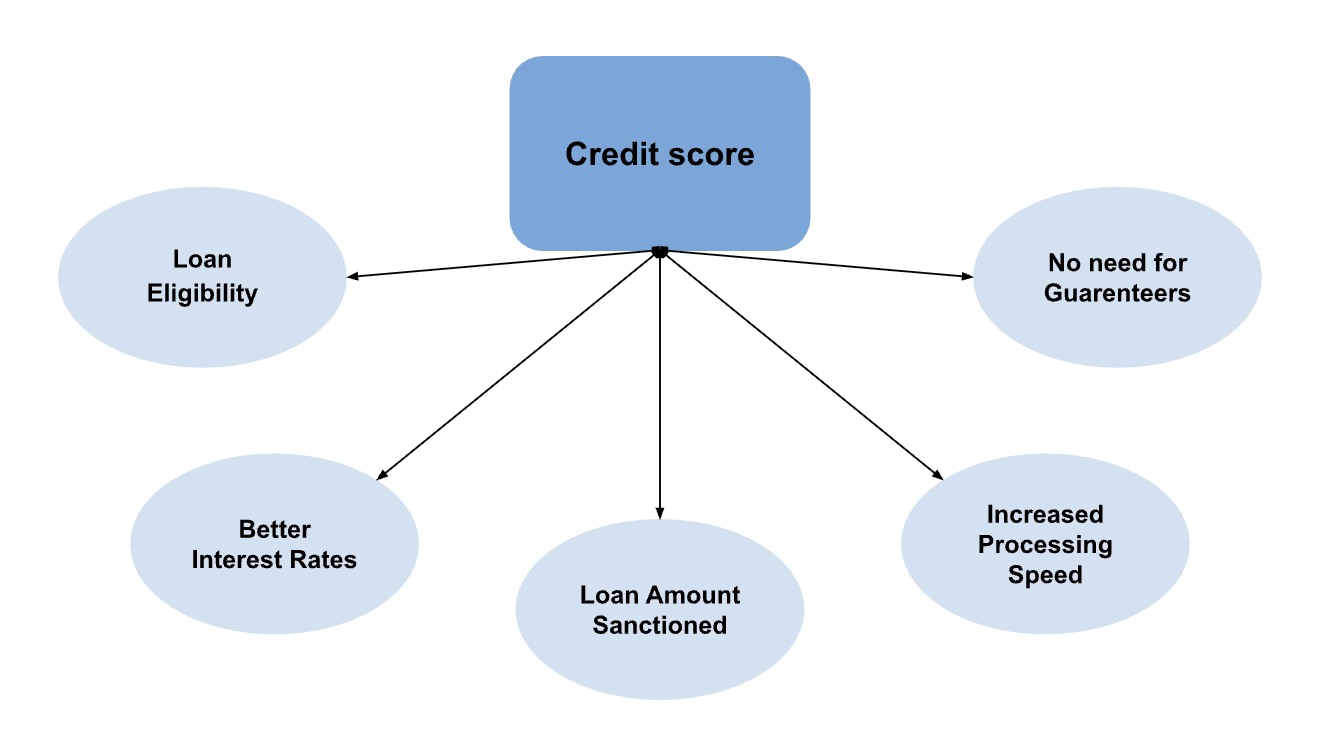

Impacts of credit score on Home Loan

Your credit score can have the following impacts on your home loan (or any other loan for that matter):

Tips to Improve CIBIL Score for Better Loan Offers

Improving the CIBIL score is a crucial aspect in improving the chances of getting approved for a home loan as well as securing a better interest rate. Following are some of the practical steps you can take to gradually build a healthier credit profile:

Pay Your EMIs and Credit Card Bills on Time

Even if you miss out on a single payment, it can affect your credit score badly. Hence, a timely repayment is necessary to build a good credit score.

Keep Credit Utilisation Below 30%

Using too much of your available credit limit depicts a financial struggle. So, maintaining a credit utilisation below 30% can help boost your score.

Don’t Apply for Multiple Loans at Once

Every time you apply for a loan, it raises a hard inquiry. Too many hard enquiries in a short period can suggest a financial struggle and can reflect badly on your credit portfolio.

Maintain a Healthy Credit Mix

A balance of secured loans (like home loans) and unsecured loans (like credit cards) credit is ideal for improving credit diversity.

Check Your CIBIL Report for Errors

Dispute any inaccuracies, like wrongly reported late payments or duplicate accounts on your credit report, as this can result in a poor credit rating.

Avoid Settling Loans or Credit Cards

Settling a loan instead of repaying it fully can mark you as a risky borrower. Paying off the debt on time can help improve your credit score.

Build a Longer Credit History

Keep older accounts active as they show long-term creditworthiness. This is helpful in the case of the CIBIL reports, as credit history constitutes a major share of report generation.

Increase Your Credit Limit (But Use Less of It)

Requesting a higher limit can help you with your needs, and not using it much improves your utilisation ratio. For example, for a card with a 1 lakh credit limit, your spendable amount with an ideal credit utilisation ratio would be ₹30,000. But if you were to increase the limit to 5 lakhs, for instance, your spendable amount would increase as well.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now