Your credit history is the record of your financial behaviour, particularly how you managed debt in the past. It plays a crucial role in determining your creditworthiness—your ability to secure loans and credit cards, even influencing job prospects. Understanding and managing your credit history is essential for financial stability and growth.

Various factors can influence your credit history. Knowing these factors can help you keep a clean credit history and maintain a good credit score. This can significantly influence your chances of getting better offers and interest rates while applying for credit.

| Credit history is a record of how you’ve used credit over time. Lenders use it to decide if you’re reliable in paying back money. A good history helps you get approved for credit and better interest rates. |

Understanding Your Credit History

Credit history consists of the record of your borrowing and repayment activities. It includes details about credit accounts, loans, payment timelines, and outstanding debts.

In India, credit information is maintained, and the credit score is calculated mainly by 4 Credit Information Companies (CICS):

- TransUnion CIBIL,

- Equifax,

- Experian, and

- CRIF High Mark,

All are regulated by the Reserve Bank of India (RBI).

Key Components of Credit History:

- Personal Information: Name, address, PAN, and other identification details.

- Credit Accounts: Details of loans and credit cards, including limits and balances.

- Payment History: Records of on-time, late and missed payments.

- Credit Enquiries: Instances when your credit report was accessed. These can be soft and hard enquiries.

Maintaining a positive credit history involves timely payments, responsible credit usage, and regular monitoring of your credit report.

The Importance of Credit History

A strong credit history is vital for various financial aspects. It reflects how reliably you’ve managed debt and financial obligations in the past. Your credit score is influenced directly by your credit history, as the credit history is one of the most important factors influencing your credit score and credit report.

Your credit history can influence your credit score, which in turn can influence your:

- Loan and Credit Approvals: Lenders use credit scores to assess the risk of lending you money. A good credit history increases your chances of being approved for loans, credit cards, and mortgages.

- Interest Rates: Applicants with strong credit histories often have higher credit scores, which can qualify them for lower interest rates.

- Rental Applications: In metropolitan cities, landlords may check credit history to determine the reliability of your rent payment.

- Employment Opportunities: Some employers review credit reports (with permission) as part of the hiring process, especially for roles involving financial responsibilities.

- Insurance Premiums: Insurers may use your credit history to determine premiums for auto and home insurance. This is done to verify your timely payment habits.

- Utility Services: A solid credit history can help you avoid security deposits when setting up utility accounts by proving that you are a highly probable applicant in terms of timely payments.

A positive credit history reflects financial responsibility, enhancing trust among lenders and other stakeholders.

A Good Credit History

A good credit history means you’ve consistently demonstrated responsible credit behaviour over time, and it’s typically reflected in a good to excellent credit score. In technical terms, this means your credit score could be anywhere between 700 and 800 if you have a very good credit history.

A good credit history is characterised by:

- Timely Payments: Consistently paying bills and EMIs on time.

- Low Credit Utilisation: Using a small portion of your available credit limit.

- Diverse Credit Mix: Managing various types of credit, like loans and credit cards.

- Minimal Hard Enquiries: Limiting the number of times your credit report is accessed for new credit.

Benefits:

- Higher Credit Scores: Reflects creditworthiness and can get you better offers.

- Better Loan Terms: Access to loans with favourable terms and conditions.

- Financial Flexibility: Easier approval for credit when needed.

- PAPL: If you are an individual with a high credit history and score, you might get accepted for pre-approved personal loans.

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

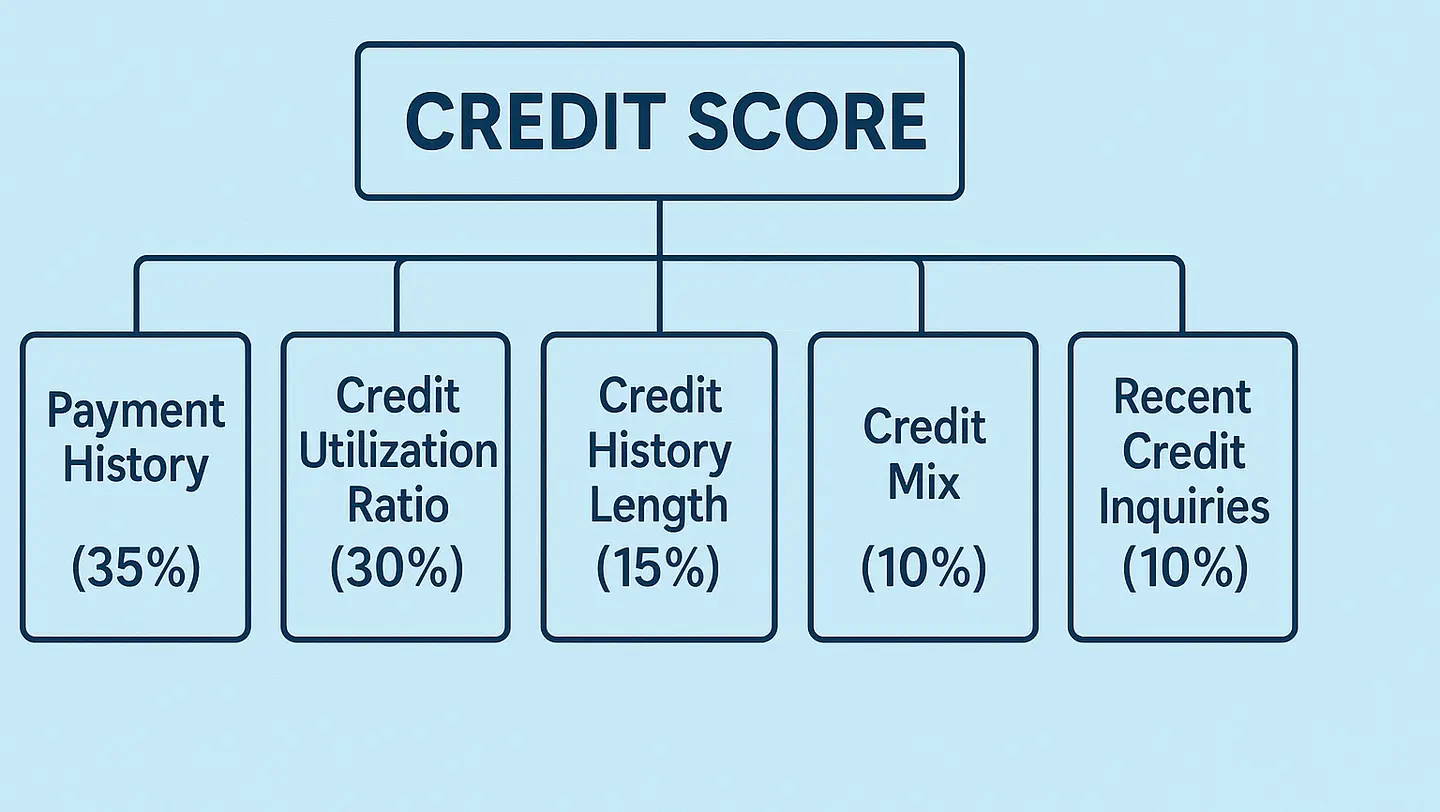

Factors Affecting Your Credit History

Several elements influence your credit history, which are also factors affecting your credit score. Knowing how each factor works can help you make informed decisions, avoid common errors, and ultimately strengthen your credit profile over time.

These are the factors that can affect your credit history:

- Payment History (35%): Timeliness of payments on credit accounts.

- Credit Utilisation (30%): Ratio of current credit balances to credit limits.

- Length of Credit History (15%): Duration of your credit accounts.

- Credit Mix (10%): Variety of credit types managed.

- New Credit Enquiries (10%): Frequency of recent credit applications.

Understanding these factors helps maintain and improve your credit history.

Tips to Improve Credit History

By enhancing your credit history, you can also improve your credit score. Improving credit score requires consistent effort, which can be achieved by developing simple habits:

- Timely Payments: Set reminders or automate payments to avoid delays.

- Reduce Outstanding Debt: Aim to pay off existing debts systematically.

- Limit New Credit Applications: Apply for new credit only when necessary.

- Monitor Credit Reports: Regularly check for inaccuracies and dispute errors.

- Maintain Older Accounts: Keeping long-standing accounts open can benefit credit history.

Implementing these practices can lead to a healthier credit profile over time.

Ways to Build Credit with No Credit History

Even if you are an individual with no prior credit history, you can still get access to credit by following certain steps. This can’t improve your credit quickly, but with careful planning and consistent efforts, you can build your credit score to a certain level, after which you can get loans based on your credit history.

- Secured Credit Cards: Backed by a deposit, they help establish credit.

- Authorised User: Being added as an authorised user for someone else’s credit card can build history.

- Credit Builder Loans: Small loans designed to be repaid over time, building credit history.

- Timely Bill Payments: Paying utilities and rent on time can indirectly influence creditworthiness.

These are some of the steps that can set the foundation for a solid credit history.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now