Ever come across the terms credit score and CIBIL score and wondered if they’re the same thing? You’re definitely not alone. They sound pretty similar and people often use them interchangeably, but there’s actually a small (but important) difference between the two credit score vs CIBIL score.

Knowing how these scores work can really help when you’re applying for a loan, trying to get a better interest rate, or just want to keep your finances in good shape. In India, most lenders look at your CIBIL Score, but that’s just one version of a credit score. There are others too, like those from Experian or Equifax, and they can vary slightly.

Let’s walk through what these scores mean, how they’re different, and why they matter.

So, What’s a Credit Score?

Your credit score is like your financial reputation. It’s a number between 300 and 900 that tells lenders how reliable you are with money, specifically, how good you are at borrowing and paying back.

Your score is based on:

- How regularly you pay your bills and EMIs

- How much of your available credit you’re using

- How long you’ve been using credit

- The variety of credit types you have

- Recent applications for new credit

Several bureaus calculate your credit score, including Experian, Equifax, CRIF High Mark and TransUnion CIBIL each with its own slightly different scoring models.

What’s the CIBIL Score Then?

The CIBIL Score is just one kind of credit score, specifically offered by TransUnion CIBIL, one of India’s major credit bureaus.

While the scoring range is the same (300–900), many banks and lenders in India prefer looking at your CIBIL score when reviewing loan applications. So if you’re applying for a loan here, your CIBIL score is likely to play a big role.

Understanding Score Ranges

Not all credit scores are created equal. Here’s how to interpret where your score stands and what it means when applying for a loan or credit card.

| Score Range | Rating | What It Means |

| 300 – 549 | Poor | Loan approval is unlikely; may be seen as a high-risk borrower. |

| 550 – 649 | Fair | You may be eligible for a loan but expect to pay higher interest rates. |

| 650 – 699 | Average | A decent chance of approval, although not always the best terms. |

| 700 – 749 | Good | Most lenders will consider you a reliable borrower. |

| 750 – 900 | Excellent | Easy approval and better interest rates. Lenders trust you. |

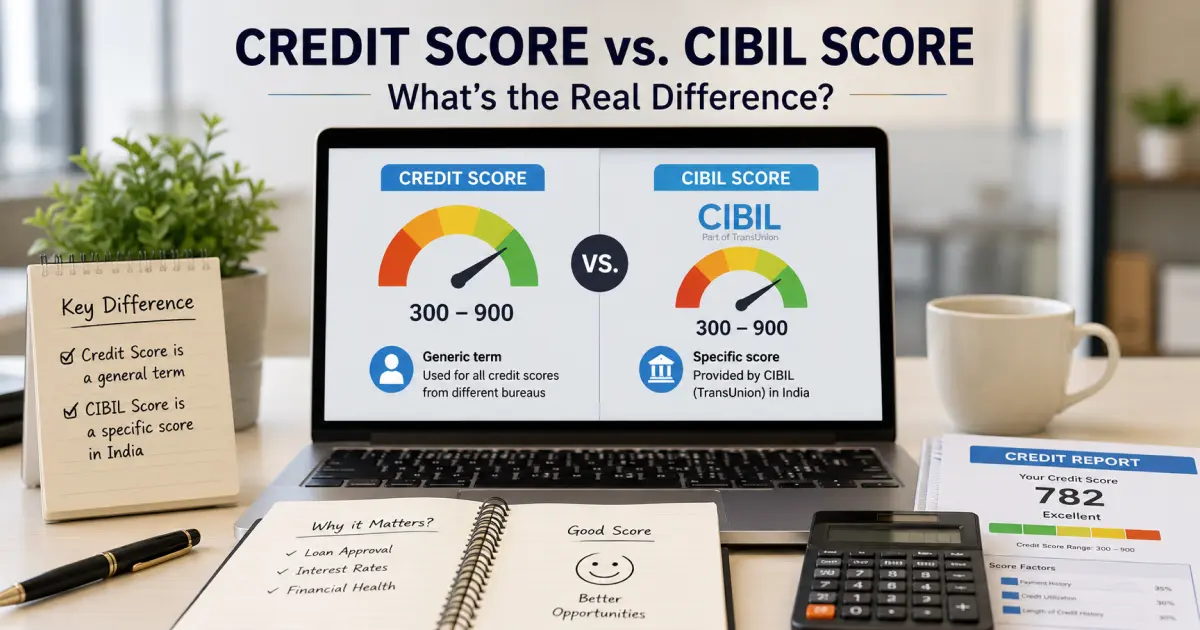

Credit Score vs. CIBIL Score

This side-by-side comparison highlights the key differences between a general credit score and the CIBIL score.

| Feature | Credit Score | CIBIL Score |

| What is it? | A general term for your creditworthiness score | A credit score specifically from TransUnion CIBIL |

| Providers | Experian, Equifax, CRIF High Mark, CIBIL | Only TransUnion CIBIL |

| Where is it used? | India and worldwide | Primarily in India |

| Score Range | 300 to 900 | 300 to 900 |

Why It’s Worth Knowing the Difference

Understanding the distinction between credit score and CIBIL score can help you:

- Know what your lender is really looking at

- Monitor your financial health across different bureaus

- Catch errors or report inaccuracies early

- Take better control of your credit journey

And if you’re planning to apply for a personal loan, knowing your credit score ahead of time can save you from surprises.

A Smart Way to Check Your Score and Explore Loans

One easy way to get started? Check your credit score for FREE. It’s a quick, reliable way to see where you stand.

And if you’re thinking of applying for a personal loan, Buddy Loan is a helpful digital platform that connects you with verified lenders based on your unique financial profile. It doesn’t offer loans directly but acts as a bridge—matching borrowers with loan offers tailored to their needs.

This can be especially useful if you’re unsure where to begin or want to explore multiple lending options in one place.

How to Check Your Score

- For CIBIL Score: Visit the official CIBIL website

- For Other Credit Scores: Use fintech apps or check with Experian, Equifax, etc.

Final Thoughts

To sum it all up: a credit score is the big-picture term. The CIBIL score is one part of that picture, especially important in the Indian context.

Knowing where you stand gives you an edge. Whether you’re taking out a loan, managing credit cards, or just keeping your finances in check, understanding your credit profile is one of the smartest things you can do.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now