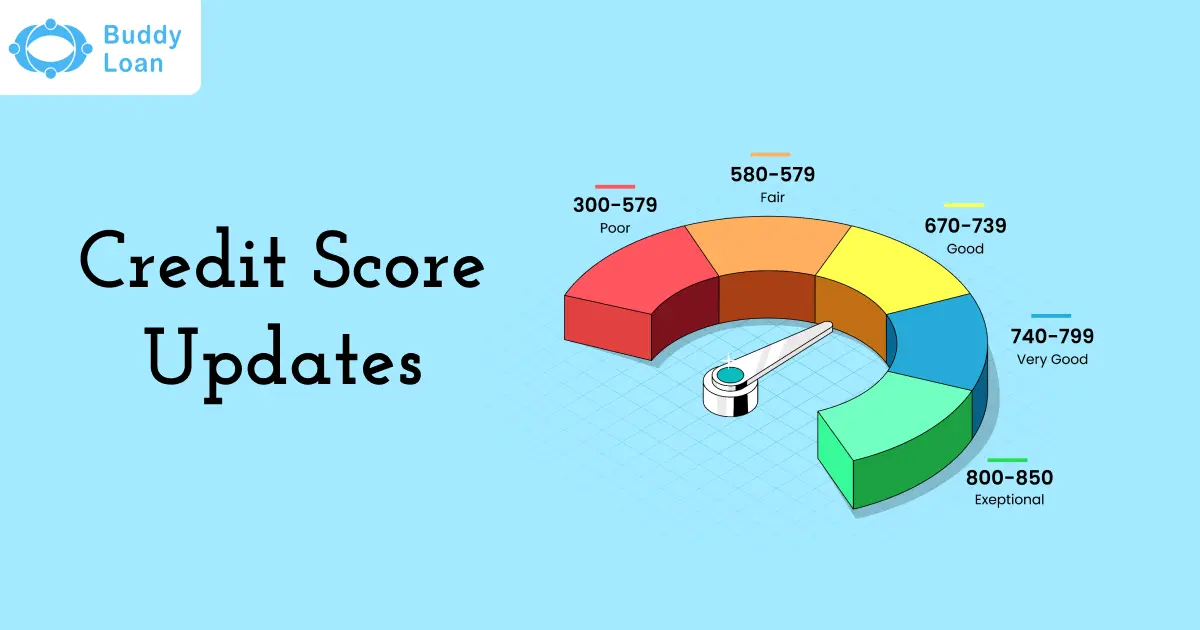

Have you ever checked your credit score after applying for a new credit card or loan, only to find it mysteriously lower? Don’t panic. The likely cause is a hard inquiry on your credit report.

Many people assume that any kind of credit check can hurt their score, but that’s not true. In reality, only hard inquiries, the ones made by lenders when you apply for new credit, can cause a dip. These are very different from soft inquiries, which are harmless.

In this blog, we’ll look at what these hard inquiries mean and how they can affect the credit score.

What Are Credit Inquiries?

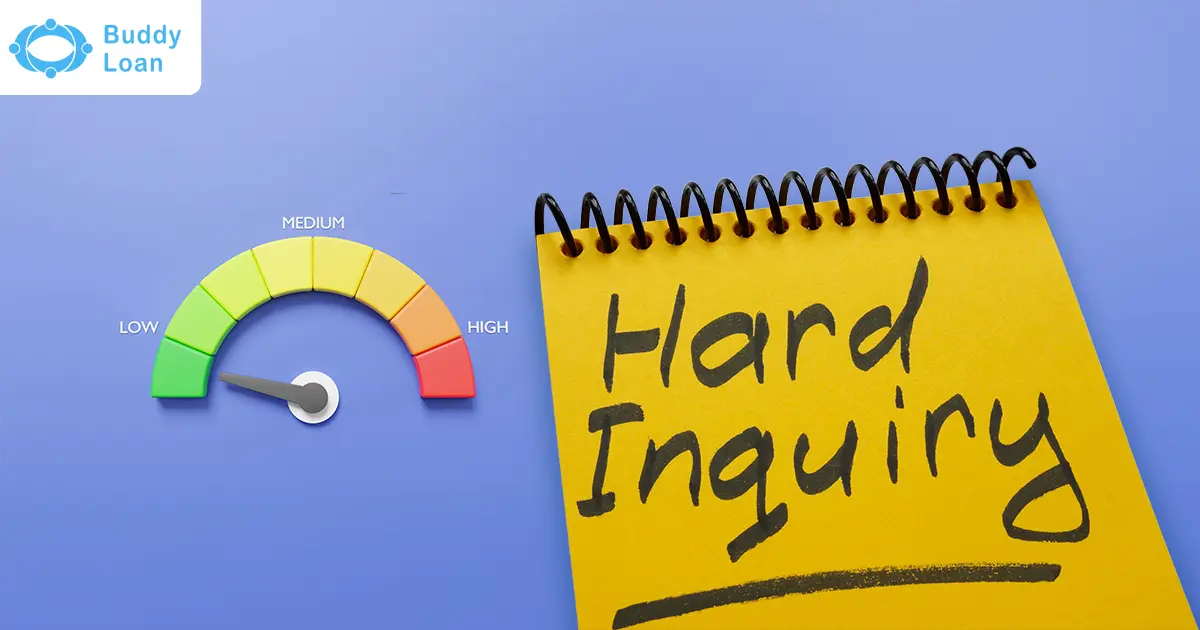

Every time someone checks your credit report, it’s called a credit inquiry, but not all inquiries are treated the same.

There are two types of credit inquiries, and only one affects your score:

- Soft Inquiry:

This happens when you check your own credit score, a company sends you a pre-approved offer, or an employer reviews your report during background checks.

Soft inquiries do not affect your credit score. - Hard Inquiry:

This happens when a lender reviews your credit because you applied for a loan, credit card, or mortgage.

Hard inquiries can lower your credit score by a few points, especially if you have many within a short time.

Why Only Hard Inquiries Affect Credit Score

Hard inquiries are important because they show lenders that you’re actively looking to borrow money. That might not sound bad, but too many inquiries in a short period can raise red flags.

One or two hard inquiries might lower your credit score by just a few points, which is usually less than 10. This small dip is temporary and often recovers within a few months. However, if you apply for several loans or credit cards back-to-back, the impact starts to add up.

Lenders may begin to wonder:

- Are you in financial trouble?

- Are you taking on more debt than you can handle?

This perception can make lenders cautious, and they may respond by denying your application or offering less favorable terms, such as higher interest rates.

In short, hard inquiries don’t just lower your score; they can influence how lenders see your financial behavior.

Suggested Read: Hard vs. Soft Credit Enquiry

How Multiple Hard Inquiries Impact You

One hard inquiry might not make a big difference, but when you stack several of them close together, the consequences start to grow.

Here’s how multiple hard inquiries can affect you:

- Drop in Credit Score

Each hard inquiry can lower your score slightly, usually by a few points. But if you have several within a short period, the dip becomes more noticeable and may take longer to recover. - Trouble Getting Approved

Lenders may see too many recent inquiries as a warning sign. It can suggest that you’re urgently seeking credit or taking on more debt than you can manage. As a result, they might deny your application or offer less favorable loan terms. - Longer-Term Visibility

Hard inquiries stay on your credit report for up to two years. The good news is their impact lessens over time, usually fading after a few months. Still, the more inquiries you have, the longer it may take for your score to bounce back.

Multiple hard inquiries don’t just affect your score—they shape how lenders judge your financial habits.

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Special Rule: Loan Shopping Windows

If you’re planning to take out a car loan, home loan, or student loan, here’s some good news: multiple hard inquiries during a short time frame may only count as one.

Credit scoring models like FICO and VantageScore understand that smart borrowers shop around. So, if you apply to several lenders for the same type of loan within a specific time window, usually between 14 and 45 days, all those hard inquiries are grouped together and treated as a single event.

This means you can compare interest rates and loan terms without hurting your credit score multiple times.

However, this rule doesn’t apply to credit cards. Every credit card application counts as a separate hard inquiry no matter how close together they are.

Key point:

Loan rate shopping won’t damage your score if done within the right window, but credit card applications always come with individual inquiry impact.

Suggested Read: New Credit Score Update

How to Protect Your Credit Score

Keeping your credit score healthy isn’t complicated; you just need to be smart about how and when you apply for credit. Here are a few easy steps you can follow:

- Apply Only When Necessary

Avoid sending out multiple credit applications at the same time. Only apply when you truly need new credit. - Be Strategic About Loan Shopping

If you’re looking for a car, home, or student loan, try to complete all your applications within a 14 to 45-day window. This helps minimize the impact of multiple hard inquiries. - Use Pre-Approval Options

Many lenders offer pre-approval checks using soft inquiries. These give you a sense of your eligibility without lowering your credit score. - Check Your Credit Report Regularly

Make it a habit to review your credit report. If you spot any unauthorized or unfamiliar hard inquiries, report them immediately and dispute errors. Keeping your report accurate is essential for maintaining a strong score.

Smart borrowing and timely checks can go a long way in protecting your financial health

Suggested Read: Tips to Achieve a Good Credit Score

On The Whole

Not all credit inquiries are harmful, but the hard ones definitely matter. They can bring your score down, affect your ability to borrow, and stay on your credit report for up to two years.

The good news? You’re in control. By understanding how credit inquiries work and making smart choices like timing your loan applications and using pre-approval tools, you can protect your credit score and build a stronger financial future.

Now that you know the difference, you can borrow smarter and keep your score in top shape.