When your CIBIL score isn’t at its best, getting a loan can feel like navigating a maze. Banks and financial institutions check your creditworthiness closely before lending and a low score can make approvals tricky. One common solution is a guarantor, someone who stands as a safety net for the lender. But do you always need one? Let’s break it down in simple, easy-to-understand terms.

What Is a CIBIL Score?

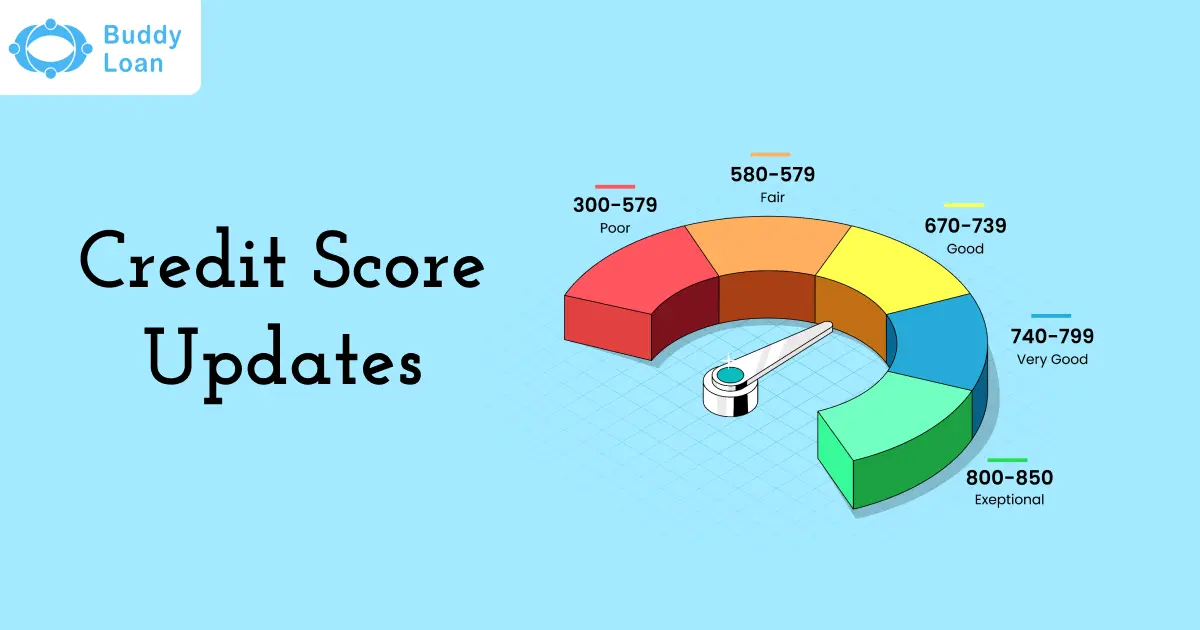

A CIBIL score is a three-digit number that reflects your credit history and repayment behaviour. Think of it as a report card for how responsibly you handle credit cards, personal loans and other borrowings. The score ranges from 300 to 900:

- 750-900: Excellent – Easy loan approval

- 650-749: Good – Moderate approval chances

- 550-649: Fair – May require additional proof or guarantor

- 300-549: Poor – Generally considered low, meaning lenders are less likely to approve a loan unless you provide a guarantor or some form of collateral

Banks use this number to gauge risk. The lower your score, the more cautious they are, as it signals past missed payments, defaults or high credit utilization.

Lenders Care About Your Credit Rating

Banks and lenders want to make sure that any money they lend will be returned on time. Your CIBIL score acts as a snapshot of your financial reliability.

- High Score: Shows you pay your bills and EMIs on time. Lenders see you as a low-risk borrower and are more likely to approve your loan quickly.

- Low Score: Signals missed payments, defaults or overuse of credit. Lenders may hesitate or impose higher interest rates to compensate for the risk.

Essentially, your credit rating is a trust meter. A strong score can save you money and time, while a low score may require extra measures, like providing a guarantor or collateral, to reassure the lender.

By understanding how lenders interpret your score, you can better plan your loan strategy and improve your chances of approval.

Who Is a Guarantor?

A guarantor is someone who agrees to take responsibility for your loan if you are unable to repay it.

- Usually, a guarantor is a close family member or a trusted friend with a good credit history and stable income.

- Their role is to assure the bank that even if your payments slip, the loan will still be repaid on time.

- Banks often check the guarantor’s financial health before approving your loan, making it clear that this person shares the responsibility for your debt.

In simple terms, a guarantor is someone who vouches for your creditworthiness. Having one can make a big difference if your CIBIL score is low or if you’re asking for a larger loan.

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Do Banks Ask for a Guarantor?

Banks don’t always require a guarantor, but certain situations make one necessary. You might need a guarantor if:

- Low CIBIL Score: If your credit history shows missed payments or a low score, lenders see you as a higher-risk borrower.

- Small or Unstable Income: Banks want to ensure you can comfortably repay the loan. If your income is irregular, a guarantor reassures them.

- Larger Loan Amounts: For bigger loans, lenders prefer extra security in case repayment becomes difficult.

- Insufficient Collateral: If you don’t have enough property or other assets to pledge, a guarantor can fill that gap.

In short, banks ask for a guarantor whenever they need extra assurance that the loan will be repaid on time. Having someone reliable back you up can make lenders more confident in approving your application.

Why a Guarantor Helps: Pros and Cons

A guarantor can be a real lifesaver if your credit score is low, but it’s not without responsibilities. Here’s a clear look at the benefits and drawbacks:

Pros

- Better Chances of Approval: With a guarantor, lenders are more likely to approve your loan even if your CIBIL score is low.

- Access to Higher Loan Amounts: Guarantors can help you qualify for larger loans that might otherwise be out of reach.

- Potentially Lower Interest Rates: Since the lender’s risk is reduced, you might get slightly better terms.

Cons

- Shared Responsibility: If you miss repayments, your guarantor becomes liable, and their credit score may take a hit.

- Strain on Relationships: Financial obligations can sometimes affect trust between you and your guarantor.

- Future Borrowing Limits: The guarantor’s own loan eligibility can be impacted because they’re linked to your loan.

Having a guarantor can significantly improve your chances of getting a loan, but it comes with serious responsibilities for both parties. Always communicate clearly with your guarantor before taking this step.

Alternatives If You Don’t Have a Guarantor

Not everyone has someone who can act as a guarantor and that’s okay. There are several ways to still get a loan even with a low CIBIL score:

- Offer Collateral

Instead of a guarantor, you can pledge an asset like property, a fixed deposit or gold. This gives the bank security, making them more willing to lend. - Apply with a co-applicant.

A co-applicant, often a spouse or family member with a stronger credit score, can improve your loan chances. Their financial profile supports yours. - Choose Lenders with Flexible Criteria

Certain banks and non-banking financial companies (NBFCs) focus on offering loans to people whose credit scores are below average - Opt for a Smaller Loan Amount

If you request a lower loan amount, banks may be less cautious, making approval easier. - Improve Your Credit Score

While this takes time, paying current EMIs, clearing outstanding debts and maintaining timely payments can gradually raise your score. Even a small improvement can make a big difference.

These strategies let you navigate the loan process without a guarantor while minimizing risk for both you and the lender.

Final Thoughts

Having a low CIBIL score doesn’t have to block your path to getting a loan. While a guarantor can increase your chances of approval and sometimes help secure better interest rates, it’s not the only way. Collateral, co-applicants, smaller loan amounts and improving your credit behaviour are all viable alternatives.

Remember, whether you have a guarantor or not, borrowing responsibly is key. Make sure you understand your repayment capacity and choose the right lender for your situation. With careful planning and the right approach, even borrowers with lower credit scores can achieve their financial goals.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now