Have you ever hesitated to check your credit score, fearing it might actually hurt it? You’re not alone. Many people believe that simply checking their credit report can lower their score. But is that really true?

Let’s clear the air. In this blog, we’ll explain when checking your credit score does and doesn’t affect it, the difference between types of credit inquiries, and why keeping an eye on your credit score is actually a smart financial move.

What Is a Credit Score Check?

A credit score check is simply a way to find out how healthy your credit history is. It helps both you and lenders understand how reliable you are when it comes to repaying loans and managing credit.

But not all credit score checks are the same. There are two main types:

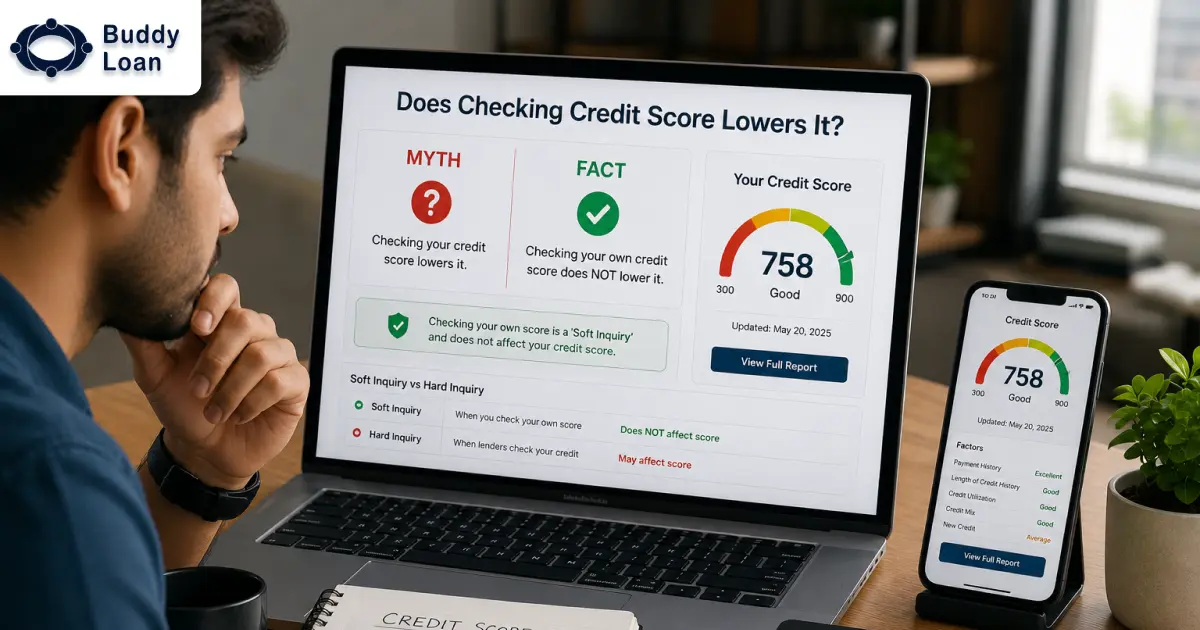

- Soft Inquiry: This happens when you check your own credit score or when it’s pulled for non-lending purposes, like background checks or pre-approved offers. Soft checks do not impact your credit score.

- Hard Inquiry: This occurs when a lender checks your score while evaluating a loan or credit card application. Hard checks may slightly lower your score, but only temporarily.

Knowing the difference is important to understand what actually affects your score, and what doesn’t.

Understanding Your Credit Score Range

In India, credit scores typically range from 300 to 900. Here’s what each score band generally indicates:

| Score Range | What It Means |

| 300–549 | Poor – High risk for lenders |

| 550–649 | Fair – May face higher interest rates |

| 650–749 | Good – Decent approval chances |

| 750–799 | Very Good – Likely to get good deals |

| 800–900 | Excellent – Strong credit profile |

The higher your score, the better your chances of securing credit with lower interest rates and more favorable terms.

Suggestion: Read More on Credit Score Range

Does Checking Your Own Credit Score Affect It?

No, checking your own credit score does not lower your credit score.

This is called a soft inquiry, and it has zero impact on your credit rating. You can check your score as many times as you like monthly, weekly, or even daily, and doing so won’t affect your credit health.

In fact, it’s smart to check your score regularly so you can spot errors, track improvements, and stay loan-ready.

What Actually Affects Your Credit Score?

While checking your own score doesn’t impact it, certain financial behaviors do. Here are some of the most common actions that can lower your credit score and why they matter:

- Your payment history is one of the biggest factors in your credit score. Missing even one EMI or credit card bill can signal risk to lenders and bring your score down.

- Using more than 30–40% of your credit limit regularly shows that you’re over-reliant on credit. Lenders prefer to see low credit utilization, which indicates better money management.

- Each time you apply for a loan or credit card, the lender makes a hard inquiry. Too many such inquiries in a short period can make you look credit-hungry, which lowers your score.

- If you’ve never taken a loan or used a credit card, you may have a low or zero credit score. Lenders find it hard to evaluate your reliability without a credit footprint.

- When you settle a loan by paying less than what you owe, it’s marked negatively on your credit report. It shows lenders that you didn’t meet the full obligation.

- Maxing out your cards, opening multiple new accounts, or closing old ones too quickly can confuse lenders and reflect poorly on your financial stability.

Checking your score doesn’t fall into any of these; consider this as just an informational action.

What Is a Hard Inquiry, and When Does It Happen?

A hard inquiry is when a lender pulls your credit report to decide whether to approve your loan or credit card application. This type of check can cause a small, temporary dip in your score by just a few points.

Hard inquiries happen when you:

- Apply for a personal loan

- Apply for a credit card

- Seek a car loan or home loan

- Request a credit limit increase

While one or two hard pulls are normal, multiple applications in a short time can signal risk and lower your score.

How Often Can You Check Your Credit Score?

There’s no limit on how often you can check your credit score. In fact, it’s recommended to check it at least once a month. This helps you:

- To monitor your progress

- It helps you catch inaccuracies or signs of fraud early

- They can improve your financial awareness

Most online platforms allow free monthly checks, and it’s completely safe.

Why You Should Regularly Check Your Credit Score

Your credit score isn’t just a number it’s a snapshot of your financial health. By checking it regularly, you stay in control and one step ahead. Here’s how it helps:

- Credit reports aren’t always perfect. A small mistake, something like a payment wrongly marked as missed, can hurt your score. Regular checks help you catch and dispute these errors before they do long-term damage.

- If someone tries to open a loan or credit card in your name, your credit report will reflect it. Monitoring your score helps you detect suspicious activity before it becomes a serious problem.

- Whether you’re new to credit or working on improving it, checking your score monthly shows you what’s working and what’s not. It helps you make smarter money moves.

- A healthy credit score opens doors. By knowing where you stand, you can apply for loans or credit cards with confidence—and get better interest rates and faster approvals.

Checking your credit score isn’t about fear, but it’s about staying financially fit.

Where Can You Safely Check Your Credit Score?

You can check your credit score through:

- RBI-approved credit bureaus (like CIBIL, Experian, Equifax, CRIF)

- Your bank or credit card provider’s app

- Trusted platforms like Buddy Loan, which offers free credit score checks and matches you with suitable lenders—all without impacting your score.

Common Myths About Checking Credit Scores

Let’s clear up some common myths:

- Myth: “If I check my credit score, it will go down.”

Fact: Soft checks don’t impact your score at all. - Myth: “Only banks can check credit scores.”

Fact: You can check your own score anytime, for free. - Myth: “Checking my score multiple times looks bad.”

Fact: Lenders don’t see your soft inquiries only hard ones.

Final Thoughts

So, does checking your credit score lower it? Absolutely not. In fact, checking your score is one of the best habits you can build for your financial future. It’s free, it’s safe, and it keeps you in control.

The more you know about your credit, the better prepared you’ll be for your next loan, credit card, or financial goal.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now