Your CIBIL score is a critical factor that determines your financial health and creditworthiness. This three-digit number, ranging from 300 to 900, serves as a snapshot of your repayment behavior and borrowing patterns. A higher CIBIL score opens doors to easier loan approvals, better interest rates, and access to premium financial products. But how is this score calculated? What factors influence it, and how can you improve it? In this blog, we’ll explore the CIBIL score calculation method, its importance, and how you can check your CIBIL score for free using tools like CIBIL calculators and online platforms.

CIBIL Score And Its Importance

A CIBIL score is a credit rating provided by TransUnion CIBIL, one of India’s leading credit bureaus. It evaluates your creditworthiness based on your borrowing history, repayment behavior, and other financial factors.

- The score ranges from 300 to 900.

- A higher score indicates better creditworthiness, while a lower score reflects potential risks for lenders.

Importance Of Having A Good CIBIL Score

1. Improves Loan Approval Chances:

Lenders prioritize borrowers with a score of 750 or higher.

2. Secures Better Interest Rates:

A high score helps you negotiate lower interest rates on loans and credit cards.

3. Demonstrates Financial Discipline:

It reassures lenders of your responsible repayment habits, making you a trustworthy borrower.

4. Offers Access to Premium Credit Products:

Premium credit cards with higher limits and exclusive benefits are often reserved for individuals with excellent credit scores.

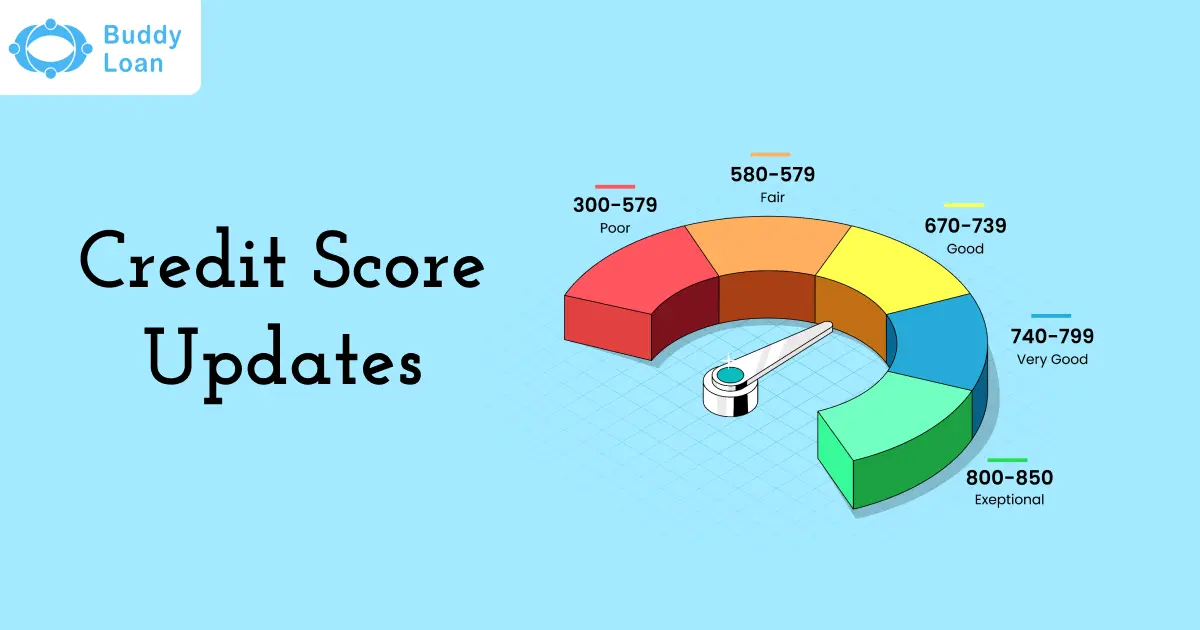

CIBIL Score Ranges and Their Meanings

| CIBIL Score Range | Meaning | Impact |

| 750-900 | Excellent | Easy loan approvals, best interest rates, and credit terms. |

| 650-749 | Good | They are likely to get loans but at slightly higher interest rates. |

| 550-649 | Fair | Limited loan options with high interest rates. |

| Below 550 | Poor | A high rejection rate; indicates financial risk. |

Calculation Of CIBIL Score

The CIBIL score calculation method involves analyzing various aspects of your credit history and financial behavior. TransUnion CIBIL uses proprietary algorithms, but the general approach is based on a weighted scoring system.

Weighted Components of CIBIL Score Calculation

| Component | Weightage | Impact on Credit Score |

| Payment History | 35% | Timely payments improve your score, while defaults and delays significantly negatively affect you. |

| Credit Utilization Ratio | 30% | Lower credit utilization (under 30%) positively impacts your score. |

| Length of Credit History | 15% | A longer credit history with consistent behavior boosts your score. |

| Credit Mix | 10% | A healthy balance of secured (home loans) and unsecured loans (credit cards) improves your score. |

| New Credit Inquiries | 10% | Frequent credit applications reduce your score due to multiple hard inquiries. |

Example of CIBIL Score Calculation

Let’s consider an example of a borrower:

- Payment History: Excellent (score component = 35/35).

- Credit Utilization: 25% usage (score component = 28/30).

- Length of Credit History: 5 years (score component = 13/15).

- Credit Mix: Balanced (score component = 8/10).

- New Credit: Minimal inquiries (score component = 9/10).

Total CIBIL Score = 35+28+13+8+9 = 93/100 (approx. 850 on a scale of 900)

This high score reflects financial discipline and enhances the borrower’s creditworthiness.

Factors Influencing CIBIL Score Calculation

Several factors determine your CIBIL score, each playing a vital role in defining your creditworthiness:

1. Payment History (35%)

- Positive Impact: Paying EMIs and credit card dues on or before the due date.

- Negative Impact: Delayed or missed payments, loan defaults.

2. Credit Utilization Ratio (30%)

- Ideal Range: Using less than 30% of your total credit limit.

- Negative Impact: High credit utilization (over 50%) indicates financial stress and reduces your score.

3. Length of Credit History (15%)

- Why It Matters: A longer credit history gives lenders more data to evaluate your repayment behavior.

- Tip: Avoid closing old credit accounts as they contribute positively to your score.

4. Credit Mix (10%)

- Balanced Portfolio: A mix of secured loans (home, car loans) and unsecured loans (credit cards) is ideal.

- Negative Impact: Over-reliance on unsecured credit lowers your score.

5. New Credit Inquiries (10%)

- Impact of Hard Inquiries: Each new loan or credit card application results in a hard inquiry, temporarily lowering your score.

- Tip: Space out your credit applications to avoid multiple hard inquiries in a short time.

Ways to Check Your CIBIL Score for Free

Checking your CIBIL score regularly is essential to monitor your credit health and identify areas for improvement. Many platforms allow you to check your score for free using simple online tools.

Steps to Check Your CIBIL Score Free of Cost

1. Visit an Authorized Platform

Go to the official CIBIL website or trusted third-party platforms like Paisabazaar, BankBazaar, or Bajaj Finserv.

Also Read: Steps to Check Your CIBIL Score on Paisabazaar

2. Enter Your Personal Details

Provide basic information such as your name, date of birth, PAN card number, and registered mobile number.

3. Complete Verification

Authenticate your identity using an OTP sent to your registered mobile number or email address.

4. Access Your Credit Report

Once verified, you can view your latest CIBIL score and a summary of your credit report.

You can also check your CIBIL Score using your PAN Card. Click on this link to see the steps for checking it.

Tips to Maintain a High CIBIL Score

Maintaining a high CIBIL score requires consistent financial discipline and strategic planning. Here’s how you can keep your score above 750:

1. Pay EMIs and Credit Card Bills on Time

Timely payments are the most significant contributor to a good credit score. Set reminders or automate payments to avoid delays.

2. Keep Your Credit Utilization Low

- Use less than 30% of your credit limit.

- Example: If your limit is ₹1,00,000, try to keep your usage below ₹30,000.

3. Avoid Frequent Credit Applications

Multiple loan or credit card applications result in hard inquiries, which can lower your score. Space out applications to minimize the impact.

4. Maintain a Balanced Credit Mix

- Have a healthy mix of secured (home loans) and unsecured (credit cards) credit.

- Avoid over-reliance on unsecured loans.

5. Monitor Your Credit Report Regularly

- Check for inaccuracies in your credit report that could negatively affect your score.

- Dispute errors immediately to protect your credit profile.

6. Avoid Closing Old Credit Accounts

Older accounts contribute to the length of your credit history, which has a positive impact on your score.

7. Don’t Default on Payments

Defaulting on loans or EMIs has a long-term negative effect. Ensure you budget carefully to meet all payment obligations.

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Common Myths About CIBIL Score Calculation

There are several misconceptions about CIBIL score calculation that can mislead borrowers. Understanding the truth behind these myths is crucial for managing your credit health effectively.

1: Checking My CIBIL Score Reduces It

- Truth: Checking your own CIBIL score is considered a soft inquiry, which does not impact your score.

- Regular checks help you stay informed and improve your financial habits.

2: Income Level Affects CIBIL Score

- Truth: Your CIBIL score is calculated based on your credit behavior, not your income level.

- Factors like timely repayments and credit utilization matter more than how much you earn.

3: Closing Credit Cards Improves Your Score

- Truth: Closing old credit cards reduces your credit history length and available credit limit, which can negatively impact your score.

- It’s better to keep accounts open and manage them responsibly.

4: A High CIBIL Score Guarantees Loan Approval

Truth: While a high score increases your chances, loan approvals also depend on other factors like income stability, existing debt, and lender policies.

5: Joint Accounts Don’t Affect My Score

Truth: If you’re a joint account holder, any defaults or delays on that account will reflect on your credit report and lower your score.

Conclusion

Your CIBIL score is a reflection of your financial habits and creditworthiness. By understanding the CIBIL score calculation method, the factors influencing your score, and the steps to check it for free, you can take charge of your financial health.

Maintaining a high CIBIL score is not a one-time effort but a continuous process of disciplined financial behavior. Regularly monitoring your credit report, paying EMIs on time, keeping your credit utilization low, and avoiding unnecessary credit applications are key strategies to keep your score above 750.

Remember, your CIBIL score is more than just a number—it’s the gateway to better loan offers, lower interest rates, and premium credit products. Start today by checking your CIBIL score using trusted tools and applying the tips shared in this guide to build a strong credit profile.

Download Personal Loan App

Get a loan instantly! Best Personal Loan App for your needs!!

Looking for an instant loan? Buddy Loan helps you get an instant loan from the best-verified lenders. Download the Buddy Loan App from the Play Store or App Store and apply for a loan now!

Download the Buddy Loan App Now! One solution to each of your financial needs at your fingertip. Scan to download now

Having any queries? Do reach us at info@buddyloan.com

Frequently Asked Questions

Q. How is a CIBIL score calculated?

A. A CIBIL score is calculated based on payment history, credit utilization, credit mix, credit history length, and recent inquiries.

Q. How is the CIBIL rank calculated?

A. The CIBIL rank is calculated for businesses, considering credit history, repayment trends, and overall financial stability.

Q. How can I calculate credit score?

A. Individuals cannot manually calculate their credit score; it is computed by credit bureaus using proprietary algorithms.

Q. What are the parameters for CIBIL score?

A. Key parameters include payment history (35%), credit utilization (30%), credit history length (15%), credit mix (10%), and recent inquiries (10%).

Q. How to get 900 CIBIL score?

A. Maintain consistent on-time payments, keep credit utilization below 30%, have a healthy credit mix, and avoid frequent loan inquiries.

Q. Is 750 a good CIBIL score?

A. Yes, a score of 750 is considered good and improves chances of loan approval at favorable interest rates.

Q. How is the CIBIL score generated?

A. CIBIL generates scores using a statistical analysis of a borrower’s credit data reported by lenders.

Q. Is a 900 credit score possible?

A. Yes, 900 is the highest possible CIBIL score, indicating impeccable credit behavior.

Q. How to increase CIBIL score immediately?

A. Clear outstanding dues, reduce credit card utilization, and rectify errors in your credit report for a quick boost.