Micro, Small, and Medium Enterprises (MSMEs) are the backbone of India’s economy, contributing significantly to employment generation, exports, and industrial growth. To support their working capital needs, expansion plans, machinery purchases, or business modernization, banks and NBFCs offer MSME loans with flexible repayment options. However, every lender assesses an applicant’s financial stability, repayment capacity, business performance, and credit profile before approving a loan.

Understanding the MSME loan eligibility criteria can help businesses prepare the right documents, improve their approval chances, and secure funding on competitive terms.

MSME Loan Eligibility Criteria

Before sanctioning an MSME loan, lenders evaluate various parameters to determine whether the business can comfortably repay the borrowed amount. Although eligibility requirements differ across financial institutions, the following criteria are commonly considered.

| Eligibility Parameter | General Requirement |

|---|---|

| Business Category | Micro, Small, or Medium Enterprise as per MSMED guidelines |

| Eligible Business Types | Sole Proprietorship, Partnership Firm, LLP, Private Limited Company, Public Limited Company, Trusts, and Registered Businesses |

| Nationality | Indian Citizen |

| Applicant’s Age | Generally 21–65 years |

| Business Vintage | Usually 1–3 years of successful operations |

| Credit Score | Preferably 700 or above |

| Annual Turnover | As per lender-specific requirements |

| Business Sector | Manufacturing, Trading, and Service |

| Income Tax Returns | Last 1–3 years (where applicable) |

| Bank Statements | Generally 6–12 months |

| Financial Statements | Profit & Loss Account and Balance Sheet (if applicable) |

| Existing Loan Obligations | Should fall within the lender’s acceptable repayment capacity |

MSME Loan Eligibility Criteria of Top Banks

Top Indian financial institutions have established specific eligibility benchmarks for MSME loans, primarily focusing on credit scores, business vintage, and financial turnover to assess creditworthiness.

| Institution Name | Minimum Credit (CIBIL) Score | Minimum Business Vintage | Minimum Annual Turnover/Income |

|---|---|---|---|

| ICICI Bank | 700+ | 1 to 3 years | ₹10 Lakhs |

| State Bank of India (SBI) | 750+ | 3+ years | ₹10+ Lakhs (varies by scheme) |

| HDFC Bank | Strong CIBIL required | 3 years | ₹40 Lakhs |

| Punjab National Bank (PNB) | 750+ | 2 years | Varies (12 months banking history) |

| Bank of Baroda (BOB) | 685+ | Established operations | Based on MSME Category |

| Canara Bank | Satisfactory CMR/CIBIL rank | 6 months to 3 years | 6 months GST returns |

Also Read: Small Business Loans | Business Loan

MSME Loan Eligibility Criteria of Top NBFCs

Leading Non-Banking Financial Companies (NBFCs) in India offer MSME loans with flexible eligibility criteria, prioritizing factors like credit scores, business vintage, and financial stability to support diverse business needs.

| NBFC Name | Minimum Credit (CIBIL) Score | Minimum Business Vintage | Minimum Annual Turnover/Income |

|---|---|---|---|

| Lendingkart | 650 | 6 to 12 months | ₹90,000 (preceding 3 months) |

| IIFL Finance | 650 to 700 | 6 to 12 months | Must be a registered MSME |

| Tata Capital | 675 | 2 years | Consistent upward turnover trend |

| SMFG India Credit | Not specified in the sources | 3 years | ₹10 Lakhs turnover |

| KreditBee | Not specified in the sources | 12 months | ₹10,000 monthly income |

MSME Loan Eligibility Calculator

Estimating your borrowing capacity before applying can help you choose a suitable loan amount and improve your chances of approval. The Business Loan Eligibility Calculator provides an estimate of the loan amount you may qualify for based on your income, existing liabilities, and repayment capacity.

Steps to Use the MSME Loan Eligibility Calculator

Follow these simple steps:

- Visit the Buddy Loan MSME Loan Eligibility Calculator.

- Enter your business and personal details.

- Provide your monthly business income or turnover.

- Enter your existing EMIs or loan obligations.

- Review the information and submit it.

- The calculator estimates the loan amount you may be eligible to borrow.

Example Calculation

Suppose your business generates a monthly income of ₹2,00,000, and your existing EMI obligations are ₹40,000.

If the lender allows a maximum EMI burden of 50% of monthly income, your repayment capacity would be:

Maximum EMI Capacity = ₹2,00,000 × 50% = ₹1,00,000

Available EMI Capacity = ₹1,00,000 − ₹40,000 = ₹60,000

Based on the selected interest rate and repayment tenure, the calculator estimates the approximate MSME loan amount you may qualify for.

Your Amortization Schedule (Yearly/Monthly)

Also Check: MSME Loan EMI Calculator

Factors Affecting MSME Loan Eligibility

Several financial and operational factors influence whether your MSME loan application is approved. Improving these areas before applying can significantly enhance your eligibility.

- Credit Score: A score of 700 or above generally improves approval chances.

- Business Vintage: Most lenders prefer businesses operating for at least one to three years.

- Annual Turnover: Consistent revenue reflects financial stability.

- Profitability: Healthy profits indicate better repayment capability.

- Cash Flow: Regular cash flow supports timely EMI repayment.

- Existing Debt: Lower outstanding liabilities improve eligibility.

- Business Registration: Udyam Registration, GST registration, and valid business licenses strengthen credibility.

- Financial Statements: Updated financial records help lenders assess business performance.

- Industry Risk: Businesses operating in stable industries generally receive better consideration.

- Repayment History: Timely repayment of previous loans positively impacts lender confidence.

Tips to Improve MSME Loan Eligibility

If your business does not currently meet a lender’s requirements, the following practices can improve your eligibility over time.

- Maintain a healthy credit score by paying EMIs and credit card bills on time.

- Register your business under Udyam to access MSME benefits.

- File Income Tax Returns and GST returns regularly.

- Keep accurate books of accounts and audited financial statements.

- Reduce existing loan obligations before applying for additional funding.

- Maintain a healthy average balance in your business bank account.

- Apply only for the loan amount your business genuinely requires.

- Avoid submitting multiple loan applications simultaneously.

- Keep all business registrations and licenses updated.

- Compare lenders to choose one that best matches your business profile.

Documents Required for MSME Loan

Providing complete and error-free documentation is vital for a smooth approval and disbursal process.

| Document Category | Required Items |

|---|---|

| KYC Documents | PAN Card, Aadhaar Card, and valid ID/Address proofs for promoters. |

| Business Proof | Udyam Registration certificate, GST Certificate, and Business PAN. |

| Financial Statements | Last 1–3 years of ITR (.xml or .pdf format) and audited Balance Sheets. |

| Bank Statements | Primary business bank statements for the latest 6 to 12 months. |

| Establishment Proof | Partnership Deed, Memorandum of Association (MOA), or Articles of Association (AOA). |

Also Read: SME Loans

Steps to Apply for a Business Loan with Buddy Loan

You can apply for an MSME Loan online through Buddy Loan by entering your basic personal, PAN, business, and loan requirement details, after which eligible offers are displayed for comparison.

- Visit the Buddy Loan Business Loan page and enter your mobile number.

- Select the required consent checkboxes to allow credit assessment and agree to the Terms of Service and Privacy Policy.

- Enter the 4-digit OTP sent to your registered mobile number.

- Fill in your personal details, including your first name, last name, personal email ID, gender, date of birth, and communication address pincode.

- Click on Continue.

- Enter your PAN number as per your PAN card.

- Select your employment type, such as self-employed business.

- Choose whether you have a GST number.

- If you have a GST number, enter your GST number, business name, business vintage, business type, business nature, and annual turnover.

- If you do not have a GST number, enter your business name, business nature, and monthly income.

- Click on Continue after adding the business details.

- Select the required Business Loan amount and choose the purpose of the loan from the dropdown menu.

- Click on Continue to submit your requirement.

- Once you submit, Buddy Loan checks available Business Loan offers based on your profile.

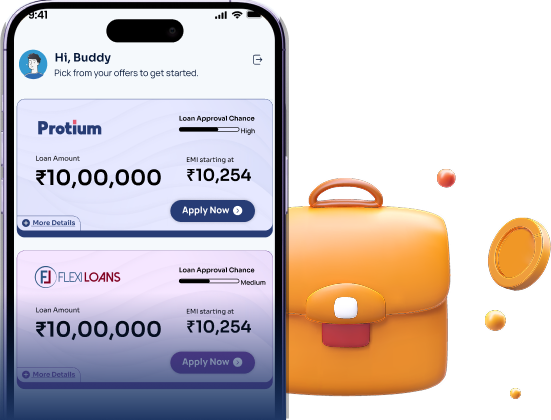

- Review the offers displayed on the screen, including loan amount, EMI, processing fee, ROI, and loan approval chance.

- Click on Apply Now for the offer that suits your requirements.

Also Read: Government Business Loans

Summary

Understanding MSME loan eligibility helps businesses prepare stronger loan applications and improves the likelihood of approval. Factors such as business vintage, turnover, profitability, repayment capacity, and credit score play a crucial role in determining eligibility. Before applying, compare different lenders, organize your financial documents, and use the Buddy Loan MSME Loan Eligibility Calculator to estimate your borrowing capacity. Choosing the right lender and applying with complete documentation can help your business access the funds it needs for sustainable growth.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now