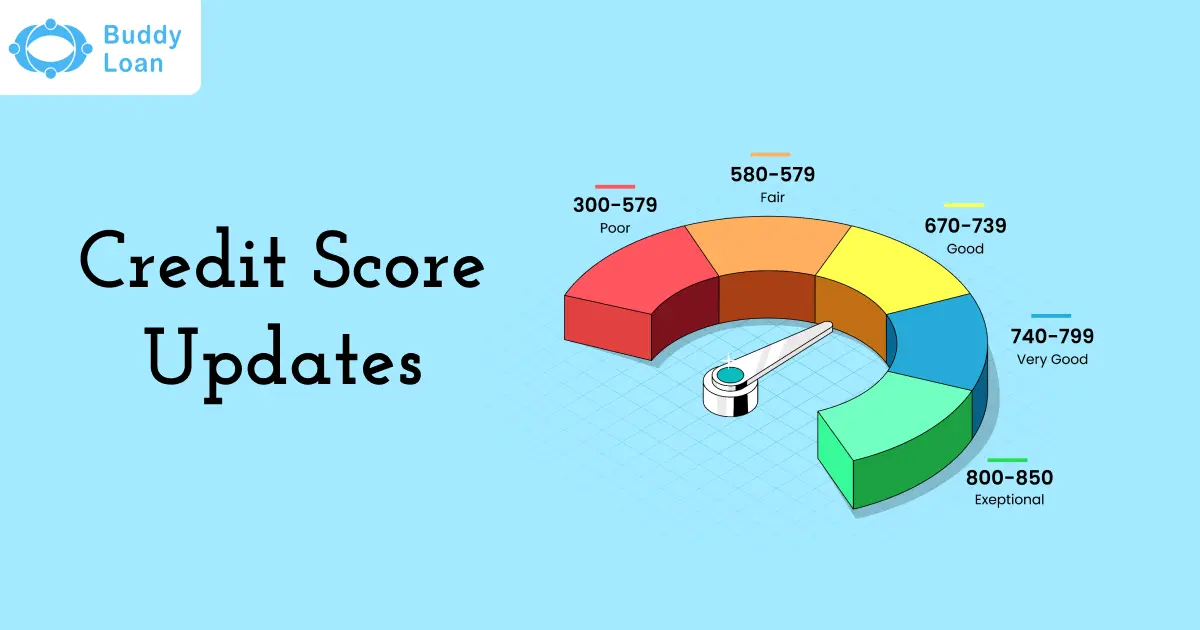

The “suit filed” status in a CIBIL report can be a significant obstacle to achieving your financial goals. It indicates that a lender has taken legal action against you for failing to meet your loan or credit obligations. This status has far-reaching consequences, including a drastic drop in your credit score, rejection of future loan applications, and difficulty accessing other financial products. However, a “suit filed” status is not irreversible. With the right approach and timely action, you can resolve the issue and remove the remark from your report. This blog will help you understand the meaning of a suit filed in CIBIL, its implications, and the steps to remove it effectively.

More About Suit Filed in CIBIL

A “suit filed” status in your CIBIL report means that a lender has initiated legal proceedings against you due to non-payment of dues. This status is reported to credit bureaus like CIBIL, signaling financial distress to other lenders.

Reasons for Suit Filed Status

- Defaulting on Loan Payments: Missing EMIs or not clearing outstanding debts for a prolonged period.

- Failure to Settle Disputes: If a borrower defaults on a negotiated settlement, the lender may escalate the issue legally.

- Irregular Payment Behavior: Patterns of delayed or partial payments that signal financial irresponsibility.

Consequences of a Suit Filed Status

When a lawsuit is filed, it triggers a series of legal and procedural implications that can significantly impact all parties involved. Understanding these consequences is crucial for navigating the complexities of the legal system effectively.

| Impact | Details |

| Significant Drop in Credit Score | Reduces your CIBIL score drastically, labeling you a high-risk borrower. |

| Loan Rejections | Lenders avoid borrowers with a “suit filed” status, rejecting loan and credit card applications. |

| Higher Interest Rates | If approved, loans may have higher interest rates due to the risk factor. |

| Long-Term Damage | The status stays on your CIBIL report for up to seven years unless resolved. |

Steps to Remove Suit Filed Status in CIBIL Report

Removing a “suit filed” status from your CIBIL report requires prompt action and careful negotiation with the lender. Follow these steps to resolve the issue:

1. Identify the Lender and Loan Account

- Review Your CIBIL Report: Identify the lender and account linked to the “suit filed” status.

- Contact the Lender: Reach out to understand the reasons for the legal action and clarify the outstanding amount.

2. Negotiate a Settlement

- Discuss Terms: Approach the lender to negotiate a repayment plan or settlement that suits your financial capacity.

- Obtain a Settlement Letter: If an agreement is reached, request a formal settlement letter outlining the terms.

3. Clear Outstanding Dues

- Pay as Agreed: Fulfill the terms of the settlement by paying the agreed amount within the specified timeline.

- Avoid Delays: Ensure timely payments to avoid further legal escalation.

4. Obtain a No Dues Certificate

- After clearing all dues, request a No Objection Certificate (NOC) from the lender. This document confirms that you have no pending liabilities.

5. Raise a Dispute with CIBIL

- Log In to the CIBIL Website: Use your account to access the Dispute Resolution section.

- Submit a Request: Provide details of the resolved case and upload supporting documents, such as the NDC and settlement letter.

- Await Verification: CIBIL will verify the information with the lender and update your report accordingly.

6. Follow Up

- Regularly check your CIBIL report to confirm the removal of the “suit filed” status.

- If it persists despite resolution, contact CIBIL and the lender for further clarification.

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Documents Required to Resolve a Suit Filed Case

Having the right documents is critical for a smooth resolution process. Here’s what you’ll need:

1. CIBIL Report

- Identify the account and lender associated with the “suit filed” status.

2. Loan or Credit Card Statement

Verify the outstanding amount and payment history.

3. Settlement Letter

Agreement between you and the lender outlining repayment terms.

4. Payment Receipts

Proof of cleared dues as per the settlement.

5. No Dues Certificate (NDC)

Confirms no pending liabilities after repayment.

6. Dispute Resolution Form

Required to submit a correction request to CIBIL.

Tips to Avoid Suit Filed Status in the Future

Preventing a “suit filed” status requires consistent financial discipline and proactive measures. Here’s how you can avoid this situation:

1. Pay EMIs and Dues on Time

- Set up automatic payments or reminders to ensure timely repayment of loans and credit card bills.

2. Monitor Your Credit Report Regularly

- Regularly check your CIBIL report for inaccuracies or early signs of financial distress.

- Dispute errors immediately to prevent unnecessary complications.

3. Avoid Over-Borrowing

- Take loans only when necessary and ensure they are within your repayment capacity.

- Maintain a credit utilization ratio below 30% to avoid excessive debt.

4. Communicate with Lenders

- If you face financial difficulties, inform your lender in advance.

- Negotiate revised terms or temporary deferments to avoid legal action.

5. Build an Emergency Fund

- Save for unforeseen circumstances to prevent defaults during financial hardships.

6. Seek Financial Counseling

- Consult a financial advisor to manage debt effectively and improve your credit behavior.

Conclusion

A “suit filed” status in your CIBIL report can have severe implications for your creditworthiness, affecting loan approvals, credit card eligibility, and overall financial credibility. However, it is not a permanent mark. By understanding the reasons behind it and following the correct steps—like negotiating with the lender, clearing dues, and raising a dispute with CIBIL—you can successfully remove the status and restore your credit profile.

To ensure long-term financial stability, adopt disciplined repayment habits, monitor your credit report regularly, and avoid over-borrowing. Remember, maintaining a good credit score isn’t just about access to loans—it’s about building trust with financial institutions and securing your financial future.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now

Having any queries? Do reach us at info@buddyloan.com

Frequently Asked Questions

Q. How to remove the ‘suit filed’ in the CIBIL report?

A. To remove the “suit filed,” resolve the dispute with the lender, pay outstanding dues, and request the lender to update CIBIL.

Q. What does “suit filed” mean in a CIBIL report?

A. “Suit filed” indicates legal action initiated by a lender due to significant default on loan repayment.

Q. Can a settled loan remove a ‘suit filed’ remark?

A. Yes, after settling the loan, you can request the lender to update the CIBIL report and remove the remark.

Q. Is it possible to dispute ‘suit filed’ in CIBIL?

A. Yes, if the “suit filed” status is incorrect, you can raise a dispute with CIBIL along with supporting documents.

Q. How long does ‘suit filed’ stay on CIBIL report?

A. Typically, it remains until the lender updates the status, but negative entries generally stay for 7 years.

Q. Will paying off debts clear ‘suit filed’ from CIBIL?

A. Paying off debts can lead to an updated status, but you must follow up with the lender to remove the remark.

Q. Can legal action remove ‘suit filed’ from CIBIL report?

A. Yes, resolving disputes legally and obtaining a no-dues certificate from the lender can help update the report.

Q. Who can help remove ‘suit filed’ from CIBIL reports?

A. Legal advisors, credit counselors, or directly coordinating with the lender can assist in resolving the issue.

Q. Does credit counseling assist with ‘suit filed’ removal?

A. Yes, credit counseling can help negotiate settlements with lenders and guide you on updating the CIBIL report.