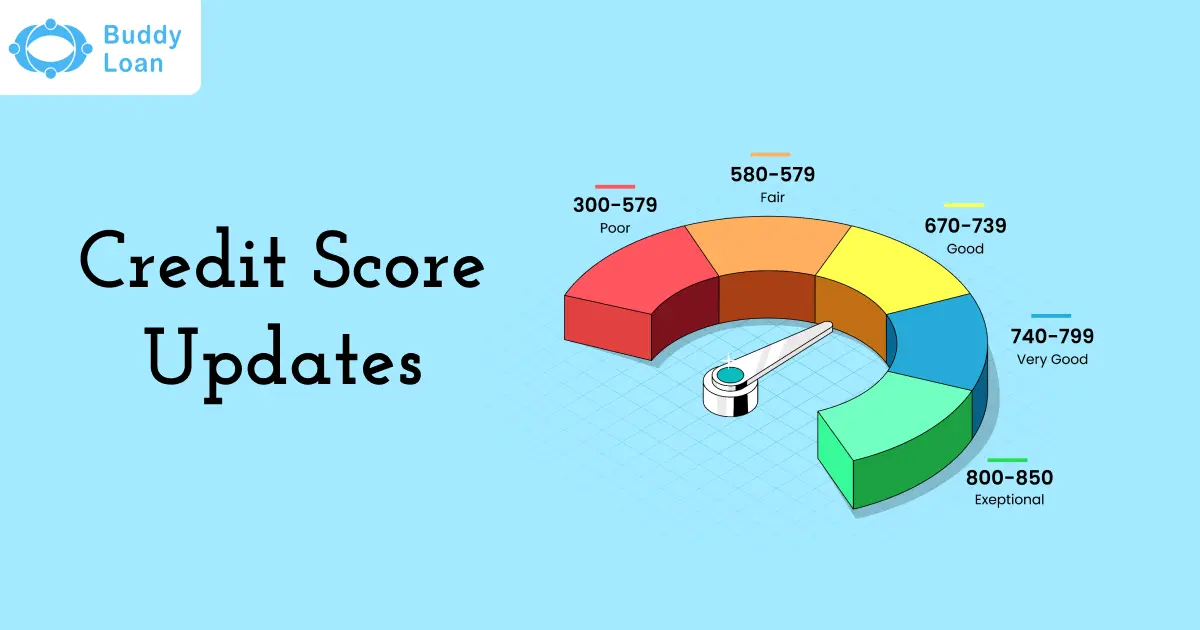

CRIF vs CIBIL are key parameters considered by lenders while granting loans. In India, banks, financial institutions, and other lending platforms widely use CRIF, CIBIL scores to evaluate your creditworthiness. These credit bureaus have data on your credit history, payments, outstanding loans, and your credit report. CRIF High Mark and CIBIL Score are two distinct entities valued between 300 and 900 points. In this blog, let’s discuss the difference between CRIF vs CIBIL.

Get Personal Loan Online Up to ₹35 Lakhs By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

What Is CRIF?

CRIF High Mark is one of India’s prominent credit information and risk management companies. It serves as a credit bureau, generating credit scores between 300 and 900.

For loan approval, scores above 700 are beneficial and lenders rely on CRIF’s credit reports to assess borrowers.

CRIF collects data from various sources, including banks, non-banking financial companies (NBFCs), and other microfinance institutions to compile these reports. This data contains the borrower’s credit history, outstanding loans, payment history, and credit scores, helping lenders evaluate risk and make informed lending decisions.

What Is CIBIL Score?

CIBIL, officially known as the Credit Information Bureau (India) Limited, stands as India’s oldest and most influential credit information bureau, established in 2000. Its primary function is to collect and manage credit information for both individuals and businesses. It generates three-digit credit scores, referred to as CIBIL scores, which range from 300 to 900.

CIBIL generates comprehensive credit reports, commonly known as Credit Information Reports (CIRs). These reports offer a detailed overview of an individual’s credit behaviour, encompassing both positive and negative aspects. Financial institutions heavily rely on these reports to assess a borrower’s eligibility for loans, determine interest rates, and establish other loan terms and conditions. The higher the CIBIL score, the more chance for loan approval.

Also Read: Guide on Credit Information Companies in India

Difference Between CRIF & CIBIL

While both CRIF and CIBIL serve the same fundamental purpose of providing credit information, there are some key similarities and differences to consider i.e.,:

Ownership and Establishment:

CIBIL: CIBIL is an Indian credit bureau, established in 2000. It was founded by the Indian Banks’ Association (IBA), leading banks and financial institutions. It is known as the TransUnion CIBIL Score or TUCS.

CRIF: CRIF High Mark is a joint venture between CRIF, an Italian company, and several Indian financial institutions. Established in 2007, called the CRIF High Mark Score.

CRIF CIBIL Score Range:

CIBIL: CIBIL scores range from 300 to 900.

CRIF: CRIF High Mark’s credit score range typically goes up to 850.

CRIF Credit Score Free Report:

CIBIL: CIBIL offers one free credit report per year to individuals. Subsequent reports may be chargeable.

CRIF: CRIF High Mark provides free credit reports to individuals once a year. Additional reports may incur a fee.

Credit Data Sources:

CIBIL: CIBIL primarily collects credit data from banks and financial institutions. It has partnerships with over 2,400 lenders across India.

CRIF: CRIF High Mark collects credit information from a wide range of sources, including banks, non-banking financial companies (NBFCs), and microfinance institutions.

Credit Report Format:

CIBIL: CIBIL’s credit reports are comprehensive and include detailed credit histories.

CRIF: CRIF High Mark provides credit reports in a user-friendly format that is easy for individuals to understand.

Credit Score Factors:

CIBIL: CIBIL scores consider factors like payment history, credit utilization, credit mix, and recent credit behavior.

CRIF: CRIF High Mark’s credit scores are influenced by factors such as an individual’s repayment history, credit utilization, and the length of credit history.

Market Presence:

CIBIL: CIBIL is widely recognized and extensively used by lenders and financial institutions throughout the country.

CRIF: CRIF High Mark is well-established in the credit industry and provides services to businesses and lenders across India.

Licensing:

CIBIL: While CIBIL is formally registered and supervised by the RBI, it is under the control of the private, unlisted corporation TransUnion.

CRIF: In contrast, CRIF is directly under the control of the Reserve Bank of India (RBI).

Want to know how to increase the CIBIL Score

Also Read: CIBIL Score Full Form

To Sum Up

Despite sharing similarities in their core functions, CRIF and CIBIL both have unique attributes, score ranges, and reporting formats. Both credit bureaus seek to promote responsible lending and borrowing, ultimately resulting in a more healthy and well-informed credit environment in India. Understanding the differences between CRIF and CIBIL can help individuals and businesses make informed decisions when it comes to accessing credit and managing their financial health.

Download Personal Loan App

Get a loan instantly! Best Personal Loan App for your needs!!

Looking for an instant loan? Buddy Loan helps you get an instant loan from the best verified lenders. Download the Buddy Loan App from the Play Store or App Store and apply for a loan now!

Download the Buddy Loan App Now! One solution to each of your financial needs at your fingertip. Scan to download now

Having any queries? Do reach us at info@buddyloan.com

Frequently Asked Questions

Q. Can CRIF and CIBIL score be different?

A. Yes, CRIF and CIBIL scores can be different because they use different scoring models and collect information from different sources.

Q. Why are CIBIL and CRIF scores different?

A. CIBIL and CRIF scores differ because they have distinct scoring models and data sources.

Q. What is the difference between CRIF report and CIBIL report?

A. The difference between a CRIF report and a CIBIL report lies in the credit information they provide and their respective scoring methods.

Q. What is a good CRIF score?

A. A good CRIF score is a score of 750 or higher, but specific score ranges can vary by lender and their criteria.

Q. Why is CRIF Score less than CIBIL Score?

A. CRIF collects information from more lenders than CIBIL, which may lead to a lower score. Also, CRIF has a more complete credit history than CIBIL.