The government launched Atal Pension Yojana (APY) as a pension scheme in India, primarily targeting at the unorganized sector. It is administered by the Pension Fund Regulatory and Development Authority (PFRDA). The scheme aims to provide a regular pension income to the subscribers/retirees during their old age/post-retirement.

Under APY, subscribers make regular contributions towards the scheme during their working years, and upon retirement, they receive a guaranteed pension amount ranging from ₹1,000 to ₹5,000 per month, solely depending on the contribution amount and the age at which the contributions start. The government guarantees the pension amount.

Individuals can avail tax exemption on their contributions towards the Atal Pension Yojana under Section 80CCD of the Income Tax Act, 1961. The maximum exemption allowed under Section 80CCD (1) is 10% of the individual’s gross total income, up to a limit of ₹1,50,000. Additionally, an extra exemption of ₹50,000 for contributions to the Atal Pension Yojana Scheme is permitted under Section 80CCD(1B).

Purpose of the Atal Pension Yojana Scheme

- Atal Pension Yojana aims to provide a reliable income source for all Indian citizens after the age of 60.

- The scheme primarily targets individuals working in the unorganized sector, including occupations such as maids, delivery personnel, and gardeners.

- The main objective is to ensure that elderly citizens do not have to worry about sudden illnesses, accidents, or chronic conditions, offering a sense of financial security.

- The scheme is not limited to the unorganized sector; it is also open to private sector employees and those working in organizations without pension benefits.

Are you looking for a personal loan?

Get Personal Loan Online Up to ₹35 Lakhs By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

APY Scheme Details & Features

The characteristics of the APY scheme are outlined as follows:

Automatic Debit

One of the key conveniences offered by the Atal Pension Yojana is the automatic debit facility, where monthly contributions are directly debited from the beneficiary’s bank account linked to their pension account. Subscribers need to maintain sufficient funds in their account to accommodate this automatic debit, as failure may result in a penalty.

Flexibility in Contributions

The pension amount receivable at the age of 60 is determined by the individual’s contributions. Different contribution levels correspond to different pension amounts. Subscribers have the option to increase or decrease their contributions once a year, allowing them to adjust the corpus amount based on their financial capacity.

Guaranteed Pension

Scheme beneficiaries have the choice to receive a periodic pension of ₹1000, ₹2000, ₹3000, ₹4000, or ₹5000, depending on their monthly contributions.

Age Criteria

Individuals between 18 and 40 years of age can choose to invest in the Atal Pension Yojana. The maximum entry age for the program is 40 years, and contributions must be made for at least 20 years. This enables college students to participate in the scheme and build a retirement corpus.

Eligibility for Atal Pension Yojana Scheme

To receive benefits from the Atal Pension Yojana, you need to meet the following APY eligibility criteria:

- You must be a citizen of India.

- Your age must be between 18 and 40.

- You should make contributions for a minimum of 20 years.

- You must have a bank account linked with your Aadhar.

- You must have a valid mobile number.

Not sure of your credit score? Check it out for free now!

Documents Required to Apply For Atal Pension Yojana Scheme

Here is a list of documents that you need to submit when applying for the APY scheme:

- The individual’s savings account should be held in a specific bank and branch.

- An APY registration form must be filled out completely.

- Aadhaar and/or Mobile Number are required.

- Information about the balance in the savings bank account is needed for the monthly contribution transfer.

APY Login Porta Registration / Login

You have the option to register for an APY account through any bank in India.

- Any Indian bank can help you with the registration process for APY through NSDL or Karvy.

- Upon successful registration, you will receive a PRAN (Permanent Retirement Account Number).

- To access your APY account, you will need to use your PRAN and the relevant APY account password.

- Alternatively, you can log in to your APY account using your PRAN and account number through the NSDL portal.

Ways to Apply for Atal Pension Yojana

There are two modes to apply for the Atal Pension Yojana: Online and Offline.

Open APY Account Online

Step 1: Open an APY account online using Net banking.

Step 2: Log into Internet banking and search for APY on the dashboard

Step 3: Choose the auto-debit facility to deduct contributions automatically until the age of 60.

Step 4: Maintain a sufficient monthly balance in your account to cover the scheme payments.

Step 5: Check with your bank for online facility availability.

Open APY Account Offline

Step 1: Visit your nearest bank branch or post office where your savings account is maintained to obtain the Atal Pension Yojana form.

Step 2: Fill in all required fields and submit the form along with a photocopy of your Aadhaar card.

Step 3: The form includes an acknowledgment section that does not require your input.

Step 4: After processing your registration application, the bank will provide you with an acknowledgment receipt.

Step 5: Upon approval, you will receive a confirmation message on your registered mobile number, so providing the correct mobile number is crucial.

You can download the APY application form from the nearest branch office of any participating bank. If available, you can also download and print the form from the official websites of the participating banks. The APY account opening form is accessible for download from the official website of the Pension Fund Regulatory and Development Authority (PFRDA).

Do you need an instant loan?

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

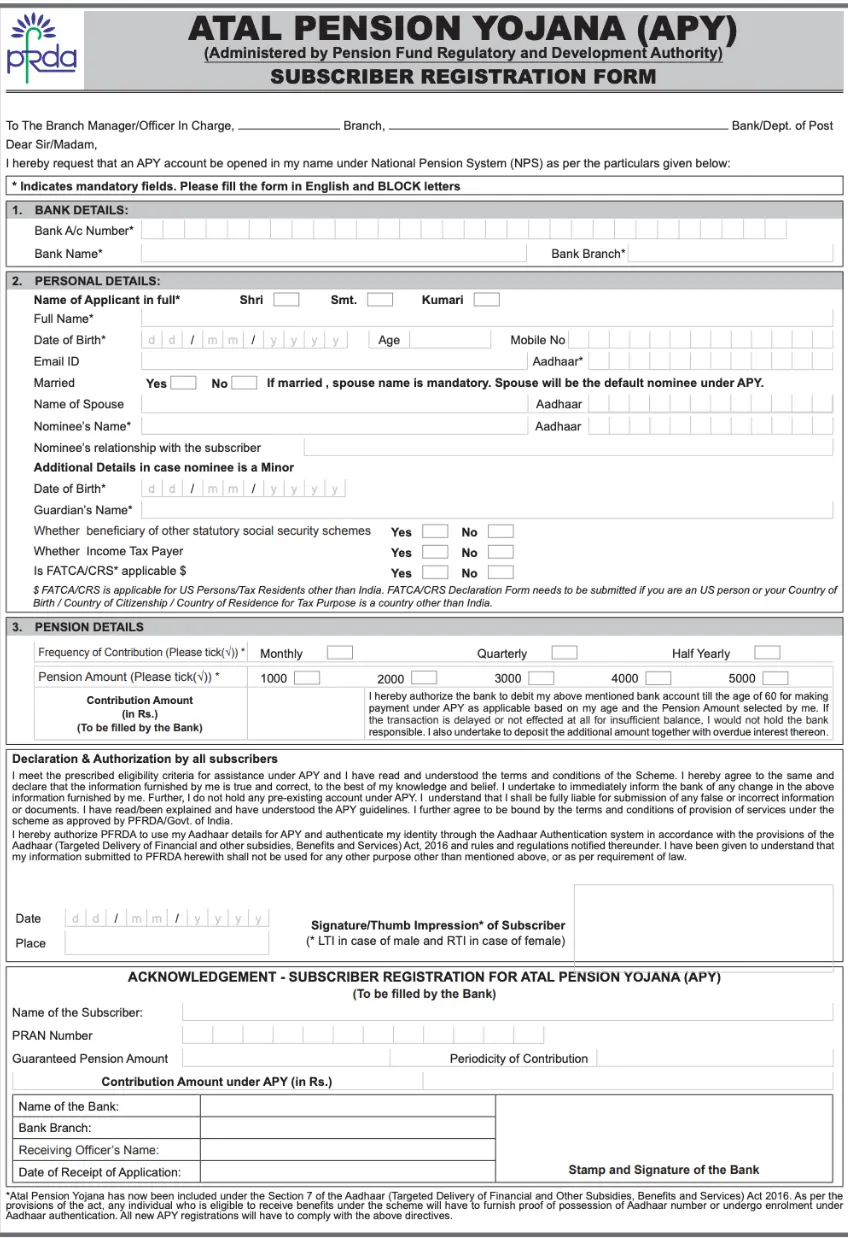

Steps to Fill Atal Pension Yojana Application Form

The Atal Pension Yojana application form consists of specific fields that must be accurately completed before submitting the form. Here is a sample of the Atal Pension Yojana subscriber registration form.

Section 1- Bank details: Includes Bank Account Number, Bank Name, and Bank Branch information.

Section 2- Personal Details: Fill in details such as Applicant’s Name, Date of Birth, Email ID, Marital Status, Spouse’s Name, Nominee’s Name, nominee’s Relationship with the Subscriber, Age, and Mobile Number of the Subscriber. Aadhar Card Details of spouse and nominee.

Section 3- Pension Details: Provide details such as selected Pension Amount – ₹1000/ ₹2000/ ₹3000/ ₹4000/ ₹5000

Section 4- Declaration & Authorization: Mention the date and place and sign the declaration form.

Section 5- Acknowledgement – Subscriber Registration for Atal Pension Yojana (APY): This section will be completed and signed/stamped by a Bank Official after processing the application. The Monthly Contribution Amount will be calculated and filled out by the bank. Upon completion, the subscriber must sign and submit the filled application form to the bank.

Atal Pension Yojana Calculator

The Atal Pension Yojana Calculator is a useful tool designed to assist individuals in planning their contributions and forecasting the pension amount they can expect to receive upon retirement. It considers variables like age, monthly contribution, and the selected pension amount.

Here are the steps to using the calculator:

Step 1: Go to the Buddy Loan website featuring the Atal Pension Yojana Calculator.

Step 2: Input your current age, influencing the monthly contribution.

Step 3: Choose your desired monthly pension from the available options, affecting the contribution calculation.

Step 4: Specify the number of years you intend to contribute to the Atal Pension Yojana.

Step 5: Click “Calculate” after entering the details to view the processed monthly contribution.

Step 6: The calculator displays the calculated monthly contribution and may offer a breakdown of contributions over the specified period.

Atal Pension Yojana Calculator

Desired Monthly Pension

(at age 60):₹1,000

Corpus Amount to Nominee

₹0

Are you in Need of personal loan?

Get Personal Loan Online Up to ₹35 Lakhs By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Fees & Charges For Maintaining APY Account

Here are the fees and charges associated with maintaining the Atal Pension Yojana scheme:

| Particulars | Charges Applicable |

|---|---|

| Registration of APY Subscriber | ₹120 to ₹150, which depends on the number of subscribers |

| Recurring Charges Per Annum | ₹100 per subscriber |

| APY Account opening charges | ₹15 per account |

| Account maintenance charges | ₹40 per account per annum |

| Investment Maintenance Fee (per annum) | 0.0075% for electronic & 0.05% for the physical segment of AUM* |

| Investment Maintenance Fee (per annum) | 0.0102% of AUM |

Note: AUM – Assets under Management

Contribution to Atal Pension Yojana Scheme

Before you apply for an APY scheme, you must know how the contribution to the scheme works. Here is a detailed breakdown:

Setting up Contributions

- To contribute to the Atal Pension Yojana, individuals need to provide their savings bank account details, mobile number, and an authorization letter allowing the bank to automatically deduct their monthly, quarterly, or half-yearly contributions through the auto-debit system.

- The due date for monthly contributions is determined by the first date of contribution, and subsequent contributions will be based on this date.

Changing Pension Payout

- Subscribers can change the pension amount once a year, in the month of April, during the contribution period.

- In case of a downgrade, the differential amount will be refunded to the contributor through direct credit to the registered bank account under APY.

- Upgrading or downgrading the APY account incurs an upfront fee of Rs. 25 charged by the bank.

Penalties and Non-Payment:

- Contributions to the Atal Pension Yojana are made through auto-debit instructions with the bank. Failure to maintain a sufficient account balance for the auto-debit may result in penalties, ranging from ₹1 to ₹10, based on the monthly contribution amount.

- If regular contributions are not made due to failure of the auto-debit instruction, the APY account may be frozen, deactivated, or automatically closed after specific periods of non-payment.

- Banks can recover the due amount until the last day of the month, and periodical mobile alerts are sent to APY subscribers to prevent late payments.

Get Quick Loan Online at Low Interest Rates!

Get Personal Loan Online Up to ₹35 Lakhs By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Atal Pension Yojana Withdrawal Process

Early withdrawal from the APY scheme is not allowed until the beneficiary reaches 60 years of age. However, exceptions may be made in cases of the beneficiary’s death or terminal illness. The possible scenarios for exiting the scheme are as follows:

- Upon reaching 60 years of age: 100% of the pension wealth will be annuitized for the subscriber.

- In the event of the subscriber’s death: The pension will be made available to the spouse, and upon the spouse’s death, the pension corpus will be returned to the nominee.

Closure & Exit of Atal Pension Yojana Account

Closure of an APY account and withdrawal from the scheme is only permitted in the event of a terminal illness or death. In the case of the subscriber’s death, the entire APY fund will be paid to the nominee as per the details provided in the APY account opening form.

Benefits of Atal Pension Yojana

Here are some of the key advantages of the Atal Pension Yojana scheme:

- Steady Income: Individuals receive a reliable source of income after reaching 60 years, enabling them to meet essential needs such as healthcare, common in old age.

- Government Backing: The pension scheme is supported by the Indian government and regulated by the Pension Funds Regulatory Authority of India (PFRDA), ensuring individuals face no risk of loss as their pension is guaranteed by the government.

- Financial Security: The scheme was introduced to alleviate the financial concerns of individuals employed in the unorganized sector, promoting financial independence in their later years.

- Spouse and Nominee Benefits: In the event of a beneficiary’s demise, their spouse becomes eligible for the scheme’s benefits, with the option to receive the corpus in a lump sum or continue receiving the same pension amount. If both the beneficiary and their spouse pass away, a nominee is entitled to the entire corpus amount.

Are you looking for a personal loan?

Get Personal Loan Online Up to ₹35 Lakhs By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Atal Pension Yojana Monthly Contribution Chart

The chart indicates the monthly contribution required for the APY scheme based on the age of entry and the desired monthly pension amount after retirement. Please note that the actual contribution amount may vary.

| Entry Age (years) | Total Years of Contribution | Monthly Contribution Amount Required | ||||

|---|---|---|---|---|---|---|

| Monthly Pension of ₹1000/ Return of Corpus of ₹1.7 lakhs | Monthly Pension of ₹2000/ Return of Corpus of ₹3.4 lakhs | Monthly Pension of ₹3000/ Return of Corpus of ₹5.1 lakhs | Monthly Pension of ₹4000/ Return of Corpus of ₹6.8 lakhs | Monthly Pension of ₹5000/ Return of Corpus of ₹8.5 lakhs | ||

| 18 | 42 | ₹42 | ₹84 | ₹126 | ₹168 | ₹210 |

| 19 | 41 | ₹46 | ₹92 | ₹138 | ₹183 | ₹228 |

| 29 | 40 | ₹50 | ₹100 | ₹150 | ₹198 | ₹248 |

| 21 | 39 | ₹54 | ₹108 | ₹162 | ₹215 | ₹269 |

| 22 | 38 | ₹59 | ₹117 | ₹177 | ₹234 | ₹292 |

| 23 | 37 | ₹64 | ₹127 | ₹192 | ₹254 | ₹318 |

| 24 | 36 | ₹70 | ₹139 | ₹208 | ₹277 | ₹346 |

| 25 | 35 | ₹76 | ₹151 | ₹226 | ₹301 | ₹376 |

| 26 | 34 | ₹82 | ₹164 | ₹246 | ₹327 | ₹409 |

| 27 | 33 | ₹90 | ₹178 | ₹268 | ₹356 | ₹446 |

| 28 | 32 | ₹97 | ₹194 | ₹292 | ₹388 | ₹485 |

| 29 | 31 | ₹106 | ₹212 | ₹318 | ₹423 | ₹529 |

| 30 | 30 | ₹116 | ₹231 | ₹347 | ₹462 | ₹577 |

| 31 | 29 | ₹126 | ₹252 | ₹379 | ₹504 | ₹630 |

| 32 | 28 | ₹138 | ₹276 | ₹414 | ₹551 | ₹689 |

| 33 | 27 | ₹151 | ₹302 | ₹453 | ₹602 | ₹752 |

| 34 | 26 | ₹165 | ₹330 | ₹495 | ₹659 | ₹824 |

| 35 | 26 | ₹181 | ₹362 | ₹543 | ₹722 | ₹902 |

| 36 | 24 | ₹198 | ₹396 | ₹594 | ₹792 | ₹990 |

| 37 | 23 | ₹218 | ₹436 | ₹654 | ₹870 | ₹1087 |

| 38 | 22 | ₹240 | ₹480 | ₹720 | ₹957 | ₹1196 |

| 39 | 21 | ₹264 | ₹528 | ₹792 | ₹1054 | ₹1318 |

| 40 | 20 | ₹291 | ₹582 | ₹873 | ₹1164 | ₹1454 |

Don’t know your credit score? You can find out for free!

APY Quarterly Contribution Chart

The Atal Pension Yojana calculation method helps determine the quarterly contribution required for the pension scheme based on entry age and desired monthly pension amount. The provided chart shows estimated values of quarterly contributions, subject to change.

| Entry Age (years) | Total Years of Contribution | Quarterly Contribution Amount Required | ||||

|---|---|---|---|---|---|---|

| Monthly Pension of ₹1000/ Return of Corpus of ₹1.7 lakhs | Monthly Pension of ₹2000/ Return of Corpus of ₹3.4 lakhs | Monthly Pension of ₹3000/ Return of Corpus of ₹5.1 lakhs | Monthly Pension of ₹4000/ Return of Corpus of ₹6.8 lakhs | Monthly Pension of ₹5000/ Return of Corpus of ₹8.5 lakhs | ||

| 18 | 42 | ₹125 | ₹250 | ₹376 | ₹501 | ₹626 |

| 19 | 41 | ₹137 | ₹274 | ₹411 | ₹545 | ₹679 |

| 29 | 40 | ₹149 | ₹298 | ₹447 | ₹590 | ₹739 |

| 21 | 39 | ₹161 | ₹322 | ₹483 | ₹641 | ₹802 |

| 22 | 38 | ₹176 | ₹349 | ₹527 | ₹697 | ₹870 |

| 23 | 37 | ₹191 | ₹378 | ₹572 | ₹757 | ₹948 |

| 24 | 36 | ₹209 | ₹414 | ₹620 | ₹826 | ₹1031 |

| 25 | 35 | ₹226 | ₹450 | ₹674 | ₹897 | ₹1121 |

| 26 | 34 | ₹244 | ₹489 | ₹733 | ₹975 | ₹1219 |

| 27 | 33 | ₹268 | ₹530 | ₹799 | ₹1061 | ₹1329 |

| 28 | 32 | ₹289 | ₹578 | ₹870 | ₹1156 | ₹1445 |

| 29 | 31 | ₹316 | ₹632 | ₹948 | ₹1261 | ₹1577 |

| 30 | 30 | ₹346 | ₹688 | ₹1034 | ₹1377 | ₹1720 |

| 31 | 29 | ₹376 | ₹751 | ₹1129 | ₹1502 | ₹1878 |

| 32 | 28 | ₹411 | ₹823 | ₹1234 | ₹1642 | ₹2053 |

| 33 | 27 | ₹450 | ₹900 | ₹1350 | ₹1794 | ₹2241 |

| 34 | 26 | ₹492 | ₹983 | ₹1475 | ₹1964 | ₹2456 |

| 35 | 26 | ₹539 | ₹1079 | ₹1618 | ₹2152 | ₹2688 |

| 36 | 24 | ₹590 | ₹1180 | ₹1770 | ₹2360 | ₹2950 |

| 37 | 23 | ₹650 | ₹1299 | ₹1949 | ₹2593 | ₹3239 |

| 38 | 22 | ₹715 | ₹1430 | ₹2146 | ₹2852 | ₹3564 |

| 39 | 21 | ₹787 | ₹1574 | ₹2360 | ₹3141 | ₹3928 |

| 40 | 20 | ₹867 | ₹1734 | ₹2602 | ₹3469 | ₹4333 |

Get an instant personal loan in minutes! Apply now!

Get Personal Loan Online Up to ₹35 Lakhs By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Atal Pension Yojana Half-Yearly Contribution Chart

The chart is based on current APY rules for half-yearly contributions over a specific period to achieve a desired pension amount at age 60. The listed contribution amounts are approximate and subject to change.

| Entry Age (years) | Total Years of Contribution | Half-Yearly Contribution Amount Required | ||||

|---|---|---|---|---|---|---|

| Monthly Pension of ₹1000/ Return of Corpus of ₹1.7 lakhs | Monthly Pension of ₹2000/ Return of Corpus of ₹3.4 lakhs | Monthly Pension of ₹3000/ Return of Corpus of ₹5.1 lakhs | Monthly Pension of ₹4000/ Return of Corpus of ₹6.8 lakhs | Monthly Pension of ₹5000/ Return of Corpus of ₹8.5 lakhs | ||

| 18 | 42 | ₹248 | ₹496 | ₹744 | ₹991 | ₹1239 |

| 19 | 41 | ₹271 | ₹543 | ₹814 | ₹1080 | ₹1346 |

| 29 | 40 | ₹295 | ₹590 | ₹885 | ₹1169 | ₹1464 |

| 21 | 39 | ₹319 | ₹637 | 956 | ₹1269 | ₹1588 |

| 22 | 38 | ₹348 | ₹690 | ₹1045 | ₹1381 | ₹1723 |

| 23 | 37 | ₹378 | ₹749 | ₹1133 | ₹1499 | ₹1877 |

| 24 | 36 | ₹413 | ₹820 | ₹1228 | ₹1635 | ₹2042 |

| 25 | 35 | ₹449 | ₹891 | ₹1334 | ₹1776 | ₹2219 |

| 26 | 34 | ₹484 | ₹968 | ₹1452 | ₹1930 | ₹2414 |

| 27 | 33 | ₹531 | ₹1050 | ₹1582 | ₹2101 | ₹2632 |

| 28 | 32 | ₹572 | ₹1145 | ₹1723 | ₹2290 | ₹2862 |

| 29 | 31 | ₹626 | ₹1251 | ₹1877 | ₹2496 | ₹3122 |

| 30 | 30 | ₹685 | ₹1363 | ₹2048 | ₹2727 | ₹3405 |

| 31 | 29 | ₹744 | ₹1487 | ₹2237 | ₹2974 | ₹3718 |

| 32 | 28 | ₹814 | ₹1629 | ₹2443 | ₹3252 | ₹4066 |

| 33 | 27 | ₹891 | ₹1782 | ₹2673 | ₹3553 | ₹4438 |

| 34 | 26 | ₹974 | ₹1948 | ₹2921 | ₹3889 | ₹4863 |

| 35 | 26 | ₹1068 | ₹2136 | ₹3205 | ₹4261 | ₹5323 |

| 36 | 24 | ₹1169 | ₹2337 | ₹3506 | ₹4674 | ₹5843 |

| 37 | 23 | ₹1287 | ₹2573 | ₹3860 | ₹5134 | ₹6415 |

| 38 | 22 | ₹1416 | ₹2833 | ₹4249 | ₹5648 | ₹7058 |

| 39 | 21 | ₹1558 | ₹3116 | ₹4674 | ₹6220 | ₹7778 |

| 40 | 20 | ₹1717 | ₹3435 | ₹5152 | ₹6869 | ₹8581 |

Return of Corpus to the Nominees & Beneficiaries of APY

If the APY subscriber passes away, the nominee or beneficiary of the subscriber will receive a payout based on the monthly pension amount chosen by the subscriber.

| Monthly Pension Amount | Return of Corpus to the nominee of the subscriber |

|---|---|

| ₹1000 | ₹1,70,000 |

| ₹2000 | ₹3,40,000 |

| ₹3000 | ₹5,10,000 |

| ₹4000 | ₹6,80,000 |

| ₹5000 | ₹8,50,000 |

Get a personal loan with ease!

Get Personal Loan Online Up to ₹35 Lakhs By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Investment Plan for the Atal Pension Yojana (APY)

The Atal Pension Yojana (APY) ensures guaranteed returns. Your money is invested in various strands, including the following:

| Type of Investment | Quantum of Investment |

|---|---|

| Government Securities | 45% to 50% |

| Term deposits of banks and debt securities | 35% to 45% |

| Equity and equity-related instruments | 5% to 15% |

| Asset-backed securities and so on | Up to 5% |

| Money Market Instruments | Up to 5% |

You can check out more on the Atal Pension Yojana Scheme from the links provided in the table below:

| SBI Atal Pension Yojana | Atal Pension Yojana Chart |

|---|---|

| Atal Pension Yojana Statement | APY Balance Check |

| APY PRAN number search | APY Calculator |

| Atal Pension Yojana Exit Policy | NPS Vs APY |

Key Points on Atal Pension Yojana Scheme

Here are some important points to consider about Atal Pension Yojana:

- Your periodic contributions will be automatically debited from your account, so make sure you have enough balance.

- You can increase your premium by visiting your bank and speaking with your manager.

- If you miss payments, a penalty of ₹1 per month for every ₹100 or part thereof will be imposed.

- If you default for 6 months, your account will be frozen, and if it continues for 12 months, it will be deactivated. If you fail to make payments for 24 months, your account will be closed and the remaining amount will be paid to you.

- Early withdrawal is only allowed in cases of death or terminal illness, with the entire amount paid to the subscriber or nominee.

- If you close the scheme before the age of 60 for any other reason, you will only receive your contributions plus earned interest, not the government’s co-contribution or its interest.