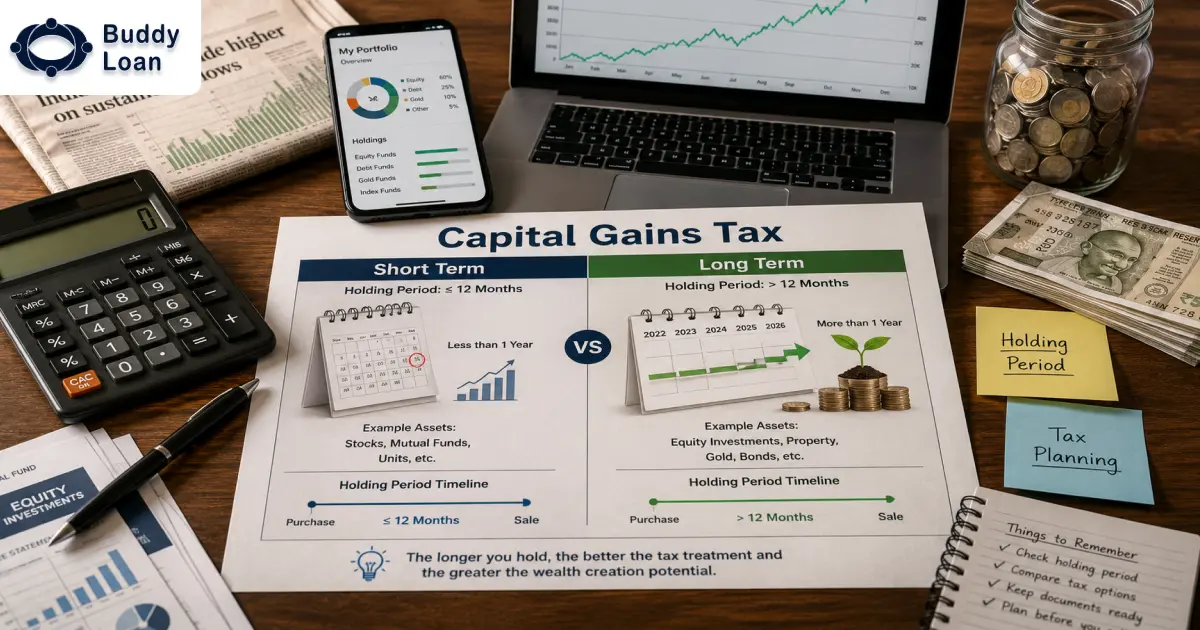

Capital gains might sound like a technical term, but they play a vital role in your financial journey, especially if you have sold shares, mutual funds, property, gold, bonds, or other investments. The profit you make from selling a capital asset is called a capital gain, and it is taxable under income tax rules.

The tax treatment depends mainly on one important factor: how long you held the asset before selling it. This holding period decides whether your gain is treated as short-term capital gain or long-term capital gain.

In this blog, we will compare short-term vs long-term capital gains tax, explain the latest 2026 rules, and help you understand how tax rates, exemptions, indexation, and asset type can affect your final tax liability.

What Is Capital Gains Tax?

Capital gains tax is the tax you pay on the profit earned from selling a capital asset. A capital asset can include investments, property, or valuable assets held for personal or financial purposes.

Common examples of capital assets include:

- Property: Land, residential house, commercial property, or building.

- Stocks and equity mutual funds: Listed shares and equity-orientated mutual fund units.

- Bonds and debentures: Listed or unlisted debt instruments, subject to specific tax rules.

- Gold and jewellery: Physical gold, ornaments, and other precious items.

- Collectibles: Artwork, antiques, and other valuable personal assets.

Capital gains are classified into two main types:

- Short-Term Capital Gains (STCG)

- Long-Term Capital Gains (LTCG)

This classification of short-term vs long-term capital gains tax matters because the tax rate, holding period, indexation benefit, loss adjustment, and exemption options differ for each type.

Short-Term Capital Gains (STCG): Definition and Tax Rates

Short-term capital gains arise when you sell a capital asset before completing the required holding period for long-term treatment. These gains often attract a higher tax rate than long-term gains.

For listed equity shares, equity-orientated mutual funds, and units of business trusts where Securities Transaction Tax, or STT, is paid, the asset becomes long-term after 12 months. If you sell before completing 12 months, the gain is treated as STCG.

For many other assets, such as land, building, gold, unlisted shares, and most non-listed assets, the holding period for long-term treatment is now generally 24 months. If the asset is sold before completing that period, the gain is short-term.

How Is STCG Taxed in 2026?

- Listed equity shares and equity mutual funds covered under Section 111A: STCG is taxed at 20% if the transfer takes place on or after 23 July 2024 and STT conditions are met.

- Transfers before 23 July 2024: The earlier 15% STCG rate applied to eligible STT-paid equity assets.

- Other assets: STCG is usually added to your total income and taxed as per your applicable income tax slab.

- Specified mutual funds, market-linked debentures, unlisted bonds, and unlisted debentures: Gains are treated as short-term capital gains in specified cases, regardless of the holding period.

Short-term capital losses can be set off against both short-term and long-term capital gains. If the full loss cannot be adjusted in the same year, it can be carried forward for up to 8 assessment years, provided you file the income tax return on time.

Example of STCG Calculation

Suppose you bought listed equity shares for Rs. 1,00,000 and sold them after 6 months for Rs. 1,40,000. STT was paid, and the sale took place after 23 July 2024.

- Sale value: Rs. 1,40,000

- Purchase value: Rs. 1,00,000

- Short-term capital gain: Rs. 40,000

- Tax at 20%: Rs. 8,000

- Health and education cess at 4%: Rs. 320

- Total tax: Rs. 8,320, subject to surcharge if applicable

Indexation: Indexation adjusts the purchase cost of an asset for inflation. It can reduce taxable gains in eligible long-term cases. However, indexation is not available for short-term capital gains.

Suggested Read: Save Tax on Short-Term Capital Gains

Long-Term Capital Gains (LTCG): Definition and Tax Rates

Long-term capital gains arise when you sell a capital asset after holding it for the minimum period required for long-term classification. LTCG usually receive more favourable tax treatment than short-term gains.

For listed equity shares, equity-orientated mutual funds, and units of business trusts, the holding period is more than 12 months. For land, building, unlisted shares, gold, and many other assets, the holding period is generally 24 months.

How Is LTCG Taxed in 2026?

- Listed equity shares and equity-orientated mutual funds: LTCG is taxed at 12.5% on gains exceeding Rs. 1.25 lakh in a financial year, subject to STT conditions.

- Land, building, gold, unlisted shares, and other long-term assets: LTCG is generally taxed at 12.5% without indexation for transfers on or after 23 July 2024.

- Land or building acquired before 23 July 2024: Resident individuals and HUFs can compare 12.5% without indexation with 20% using indexation and apply the more beneficial tax outcome.

- Debt-orientated specified mutual funds: Units covered under Section 50AA are treated as short-term capital assets in specified cases and taxed at applicable slab rates.

Example of LTCG Calculation: Sale of Real Estate

Assume a resident individual bought a residential property in FY 2019-20 for Rs. 25,00,000 and sold it in FY 2025-26 for Rs. 50,00,000. Since the property was acquired before 23 July 2024, the taxpayer can compare both methods if eligible.

Option 1: Tax at 12.5% Without Indexation

- Sale price: Rs. 50,00,000

- Original purchase price: Rs. 25,00,000

- Long-term capital gain: Rs. 25,00,000

- Tax at 12.5%: Rs. 3,12,500

- Cess at 4%: Rs. 12,500

- Total tax: Rs. 3,25,000, subject to surcharge if applicable

Option 2: Tax at 20% With Indexation

- Purchase price: Rs. 25,00,000

- CII for FY 2019-20: 289

- CII for FY 2025-26: 376

- Indexed cost: Rs. 25,00,000 x 376 / 289 = Rs. 32,52,595

- Indexed long-term capital gain: Rs. 50,00,000 – Rs. 32,52,595 = Rs. 17,47,405

- Tax at 20%: Rs. 3,49,481

- Cess at 4%: Rs. 13,979

- Total tax: Rs. 3,63,460, subject to surcharge if applicable

In this example, the 12.5% option without indexation gives a lower tax outgo. However, this may change depending on the year of purchase, sale value, improvement cost, and inflation adjustment.

Example of LTCG Calculation: Listed Equity Shares

Suppose you bought listed equity shares for Rs. 2,00,000 and sold them after more than 12 months for Rs. 4,00,000. STT conditions are satisfied.

- Sale value: Rs. 4,00,000

- Purchase value: Rs. 2,00,000

- Long-term capital gain: Rs. 2,00,000

- Annual exemption under Section 112A: Rs. 1,25,000

- Taxable LTCG: Rs. 75,000

- Tax at 12.5%: Rs. 9,375

- Cess at 4%: Rs. 375

- Total tax: Rs. 9,750, subject to surcharge if applicable

Long-Term Capital Gains Tax Exemptions in 2026

You can claim exemptions on eligible long-term capital gains if you reinvest the gains or sale proceeds as per the conditions given under the Income Tax Act.

- Section 54: Available to individuals and HUFs on sale of a long-term residential house property if the capital gain is invested in another residential house in India within the specified time. The exemption is subject to conditions and the Rs. 10 crore cap.

- Section 54F: Available on sale of any long-term capital asset other than a residential house, if the net sale consideration is invested in a residential house in India. The exemption is proportionate if only part of the sale consideration is reinvested.

- Section 54EC: Available on long-term capital gains from land or buildings if the taxpayer invests in specified bonds such as NHAI, REC, HUDCO, IREDA, or other notified bonds within 6 months. The investment limit is Rs. 50 lakh.

- Section 54B: Available on sale of agricultural land if the taxpayer reinvests in another agricultural land within 2 years, subject to conditions.

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Short-Term vs Long-Term Capital Gains Tax: Key Differences

Understanding how capital gains are categorised can help you plan your investments more efficiently. The table below gives a quick comparison based on the latest capital gains rules applicable in 2026.

| Parameter | Short-Term Capital Gains | Long-Term Capital Gains |

|---|---|---|

| Meaning | Profit from selling an asset before completing the required long-term holding period. | Profit from selling an asset after completing the required long-term holding period. |

| Holding Period for Listed Equity and Equity Mutual Funds | 12 months or less | More than 12 months |

| Holding Period for Land, Building, Gold, and Many Other Assets | Less than 24 months | 24 months or more, depending on asset category |

| Tax Rate for Listed Equity with STT | 20% for transfers on or after 23 July 2024 | 12.5% on gains above Rs. 1.25 lakh |

| Tax Rate for Other Assets | Usually taxed as per applicable slab rate | Generally 12.5% without indexation for transfers on or after 23 July 2024 |

| Indexation Benefit | Not available | Generally removed, except grandfathering relief for eligible resident individuals and HUFs selling land or building acquired before 23 July 2024 |

| Loss Set-Off | Can be adjusted against STCG and LTCG | Can be adjusted only against LTCG |

| Exemptions | Usually not available for short-term gains | Available under sections such as 54, 54F, 54EC, and 54B, subject to conditions |

| Common Assets | Shares, mutual funds, property, gold, or other assets sold early | Shares, mutual funds, real estate, gold, or other assets held beyond the long-term threshold |

Suggested Read: Save Long-Term Capital Gains Tax

Why This Matters

The difference between short-term vs. long-term capital gains can directly affect how much tax you pay. For example, selling listed equity shares within 12 months may attract 20% STCG tax. Holding them for more than 12 months may move the gain to LTCG treatment, where only gains above Rs. 1.25 lakh are taxed at 12.5%.

The same logic applies to property, gold, and other assets, but with different holding periods and tax treatment. A sale made too early may push the gain into the short-term category and increase the tax outgo. A planned sale can help you use lower rates, exemption options, or loss set-off more effectively.

Pro Tip for 2026

Before selling a high-value asset, check three things: the holding period, the applicable tax rate, and the exemption options. If you are selling land or building acquired before 23 July 2024, compare the 12.5% tax without indexation with the 20% tax using indexation if you are eligible for the grandfathering benefit.

For equity investments, remember that the Rs. 1.25 lakh LTCG exemption applies to eligible long-term gains under Section 112A in a financial year. For specified mutual funds and certain debt instruments covered under Section 50AA, do not assume LTCG treatment just because you held the asset for a long time.

Final Thoughts

Choosing short-term vs long-term capital gains really depends on your financial goals, asset type, and investment horizon. The 2026 capital gains rules make the distinction even more important because the tax rates, holding periods, and indexation treatment have changed from earlier rules.

If you regularly trade in stocks or mutual funds, prepare for short-term capital gains tax wherever applicable. If your focus is long-term wealth creation, holding the asset beyond the required period can help you access more favourable tax treatment.

For property and other high-value assets, do not rely on rough calculations. Compare both available tax methods where eligible; check exemption options, and keep purchase documents, improvement bills, sale agreements, and investment proof ready. A small planning step before selling can reduce tax errors and help you make better financial decisions.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now