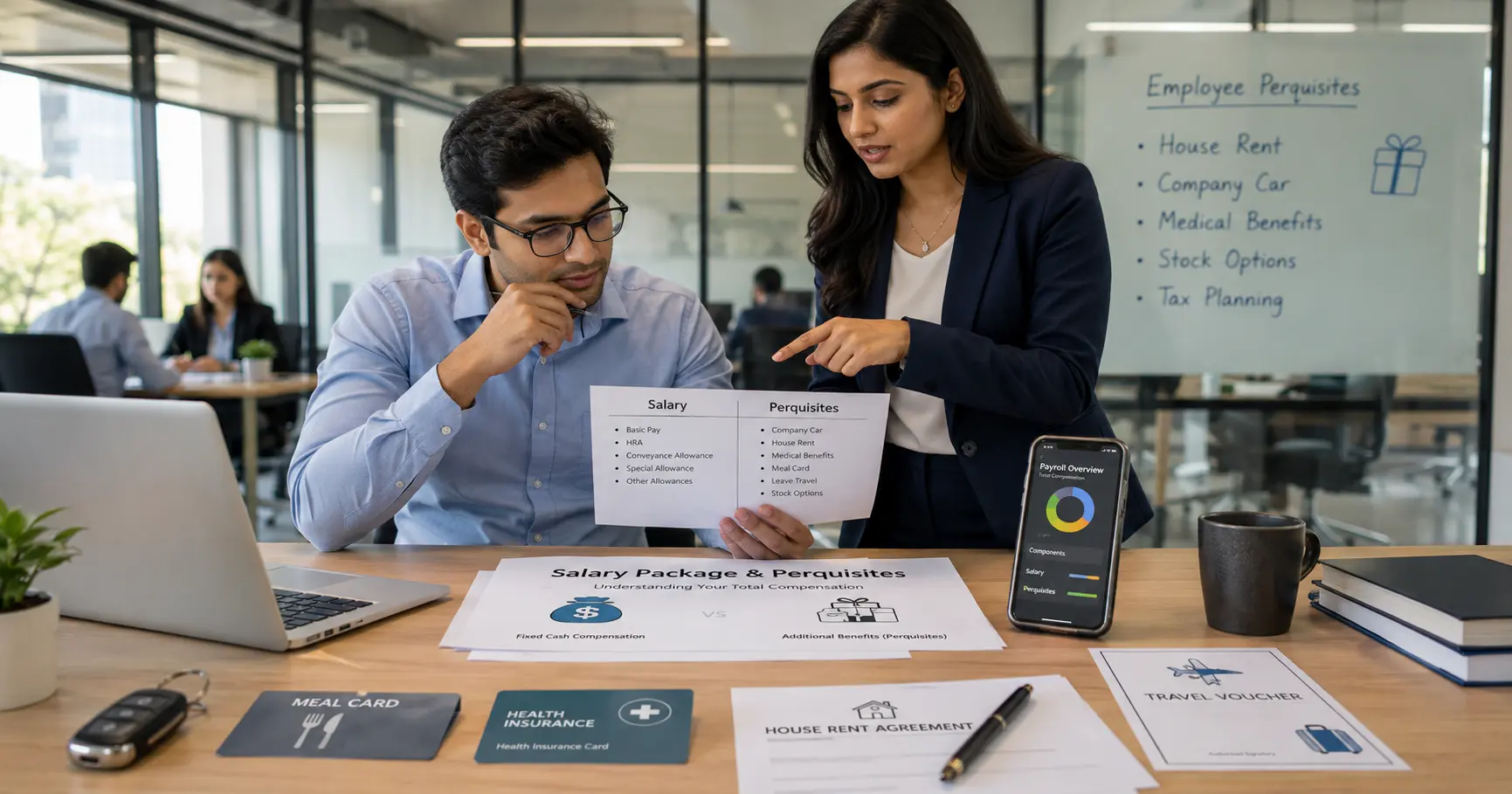

When discussing a salary package, the focus often remains on the basic pay. But there’s more to what you receive from your employer—benefits like rent-free accommodation, company cars, or even meal vouchers. These benefits are called perquisites or fringe benefits, and under Indian tax laws, many of them are taxable.

This guide will walk you through everything you need to know about perquisites, how they are taxed, how they are valued, and what it means for you as an employee.

What Are Perquisites?

Perquisites, as defined under Section 17(2) of the Income Tax Act, 1961, refer to any non-monetary benefits provided by an employer to an employee in addition to the regular salary. These benefits may be taxable or exempt depending on the type of perk and the employee’s role.

They are essential benefits in kind that enhance an employee’s overall compensation but are not always in the form of direct cash.

What Qualifies as a Perquisite?

Perquisites are non-cash benefits provided by employers in addition to salary. These can be taxable or exempt depending on usage and employee status. Common examples include:

- Rent-free or concessional accommodation: Company-provided housing or hotel stays at reduced rates.

- Company cars with fuel/driver: Vehicles provided for personal or mixed-use, including associated costs.

- Interest-free or concessional loans: Personal, housing, or education loans offered below-market interest rates.

- Club memberships and gym access: Recreational and fitness perks paid by the employer.

- Household help: Employer-covered salaries for domestic staff like drivers, cooks, or maids.

- Laptops, phones, internet: Devices or reimbursements, tax-free if used solely for work.

- Health insurance and medical reimbursements: Employer-paid premiums or expense coverage, partly exempt.

- Stock options and sweat equity: Shares given at discounted rates, tax based on fair market value at the time of vesting or exercise.

Also Read: Income Tax Rules April 2026

Types of Perquisites

Perquisites are broadly classified into three categories:

1. Taxable for All Employees

These are benefits that are taxable regardless of the employee’s designation or income level.

- Rent-free or concessional accommodation

- Company cars used for personal purposes

- Reimbursement of personal expenses

- Interest-free or low-interest loans

- Payment of personal obligations such as electricity bills or credit card dues

- Holiday expenses are borne by the employer

2. Tax-Free Perquisites

These are benefits that are completely exempt from tax under specific conditions.

- Laptops, mobile phones, and internet used for official purposes

- Refreshments served during office hours

- Employer’s contribution to superannuation fund (within prescribed limits)

- Health insurance premiums paid by the employer

- Education facilities provided to children (within limits)

3. Taxable Only for Specified Employees

As per Rule 3 of the Income Tax Rules, certain perquisites are taxable only for specified employees, which include:

- Directors of a company

- Employees having substantial interest (20% or more equity shareholding)

- Employees whose monetary salary exceeds ₹50,000 in a financial year

Benefits like domestic help, gardening, or sweeper services fall under this category.

Valuation of Perquisites

Perquisites are taxed based on their fair market value or as per rules laid out under Rule 3 of the Income Tax Rules, 1962.

1. Rent-Free Accommodation

- Government employees: License fee as per government rules

- Private sector: Valued at 7.5% to 15% of salary depending on city population

- Furnished house: Add 10% of furniture cost annually

2. Company Car

- Used exclusively for personal purposes: Full cost borne by employer is taxable

- Partly official and partly personal use: Fixed value added to salary

- Up to 1.6L engine: ₹1,800/month

- Above 1.6L engine: ₹2,400/month

- Add ₹900/month if the driver provided

3. Interest-Free Loans

- Taxable on the difference between the interest charged and the prevailing SBI rate

- Loans up to ₹20,000 are generally exempt

4. Sweeper, Gardener, Cook

- Value equals the salary paid by the employer to these workers.

5. Education Facilities

- Exempt if provided on employer’s premises and up to ₹1,000 per child per month

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

How Are Taxes on Perquisites Calculated?

The value of taxable perquisites is added to your total income under the head ‘Salaries’. Your employer is responsible for calculating the perquisite value and deducting TDS (Tax Deducted at Source) accordingly.

The perquisite tax is usually computed using the average rate of income tax applicable to the employee. This ensures a fair tax deduction and simplifies year-end tax filing.

| Example:

Let’s say an employee, Karan, earns a total salary of ₹8,00,000 annually. His employer provides additional non-monetary perquisites worth ₹1,00,000, such as rent-free accommodation or a company car. Step-by-Step Tax Calculation: Total taxable income (salary + perquisites) = ₹8,00,000 + ₹1,00,000 = ₹9,00,000 Income tax on ₹9,00,000 (under the old regime, for FY 2024–25):

Health & education cess @4% = ₹3,700 Total tax liability = ₹92,500 + ₹3,700 = ₹96,200 Average tax rate = ₹96,200 / ₹9,00,000 × 100 = 10.69% Tax on perquisites (₹1,00,000) = 10.69% of ₹1,00,000 = ₹10,690 Monthly TDS on perquisites = ₹10,690 / 12 = ₹891 Therefore, Karan’s employer must pay ₹891 per month as TDS on the ₹1,00,000 worth of taxable perquisites. This amount ensures that perquisite taxes are settled evenly throughout the year without a year-end surprise. |

Suggested Read: India’s New Tax Era

Perquisite Tax Planning Tips

- Maintain documentation for official use of laptops, internet, or phones to claim exemptions

- Use concessional housing or loans wisely, understanding the tax cost

- Take advantage of fully exempt perks like health insurance or education allowance

- Opt for salary restructuring if possible to maximize tax-free components

Perquisite Tax: Proposed Changes in Budget 2025

The government has proposed important updates to make tax-free benefits more accessible to salaried individuals. One key change relates to perquisites linked to medical travel abroad:

- Current Rule: Expenditure incurred by an employer for travel outside India for medical treatment of an employee or a family member is exempt from tax only if the employee’s gross total income is not more than ₹2 lakh.

- Proposed Change: The qualifying income limit will be increased, allowing more employees to avail of this perquisite tax-free.

This adjustment reflects the rising cost of healthcare and aims to reduce the tax burden for middle-income earners seeking medical care abroad.

These updates are expected to take effect from April 1, 2026, once the Budget 2025 proposals are implemented.

Final Thoughts

Perquisites are a key part of compensation packages in today’s job market. While they provide added comfort and value, understanding their tax implications helps you make informed financial decisions. Whether you’re negotiating a job offer or reviewing your Form 16, knowing what’s taxable and what’s not can make a significant difference in your take-home income.

If you’re ever in doubt, consult a tax advisor or refer to government notifications for the latest updates.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now