In India, long-term capital gains (LTCG) tax plays a crucial role in financial planning for investors. When you sell certain assets after holding them for a specified period, your profits may be classified as long-term capital gains and taxed at preferential rates.

Understanding how LTCG is calculated and how it applies across various asset types is essential to reduce your tax burden and plan investments wisely.

This blog takes you through all about long-term capital gains and how you can calculate them.

Understanding Long-Term Capital Gains (LTCG)

When you sell an asset like stocks, real estate, or mutual funds for more than you paid for it, you make a capital gain. If you held that asset for more than a year, your gain is considered a long-term capital gain (LTCG) and includes a specific tax rate.

These gains apply to a wide range of investment assets, and understanding how they are categorized can have a major impact on your tax strategy. Holding assets for longer not only allows for potential market growth but also helps minimize tax due to favorable rates.

In India, the holding period to classify an asset as long-term depends on the type of asset:

- Listed equity shares and equity-oriented mutual funds: More than 12 months

- Unlisted shares and real estate: More than 24 months

- Debt mutual funds, bonds, and other assets: More than 36 months

Assets That Qualify for Long-Term Capital Gains (LTCG)

Here are the assets that can be considered as Long-Term Capital gains:

- Stocks

- Bonds

- Mutual funds

- Real estate (except your primary home, under certain conditions)

- Collectibles (like art or rare coins, though taxed differently)

Suggested Read: Tips to Save on Long-Term Capital Gains

How to Calculate Long-Term Capital Gains Tax (LTCG) In India

Here are the steps you can follow to calculate your long-term capital gains (LTCG):

- Check if it’s a long-term gain: Make sure you held the asset for the required time, like over 1 year for shares or over 2 years for property, to qualify as LTCG.

- Calculate the sale amount: This is the total money you received from selling the asset.

- Figure out the indexed purchase cost: Adjust the original purchase price for inflation using the formula:

(Purchase Price × CII of sale year ÷ CII of purchase year). - Add cost of improvements: Include major repair or upgrade costs, also adjusted for inflation, if any.

- Subtract selling expenses: Deduct costs like brokerage, legal fees, stamp duty, or registration charges.

- Apply the LTCG formula: Final gain = Sale Price − (Indexed Cost + Indexed Improvements + Selling Expenses).

- Calculate the tax: Pay 10% tax on gains above ₹1 lakh for stocks/mutual funds, and 20% tax with indexation for property, gold, or other assets.

Get Personal Loan Online Up to ₹35 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Long-Term Capital Gains Tax Calculation Example

Let’s go through some examples to know how is long-term capital gains tax is calculated.

Example 1: Equity Mutual Funds

Suppose you invested ₹2,00,000 in an equity mutual fund in April 2023 and sold your units for ₹4,00,000 in May 2025, after holding them for more than 12 months.

Sale value: ₹4,00,000

Purchase value: ₹2,00,000

Capital gain: ₹4,00,000 − ₹2,00,000 = ₹2,00,000

Exempt LTCG limit: ₹1,25,000 (no tax on gains up to this amount in a financial year)

Taxable LTCG: ₹2,00,000 − ₹1,25,000 = ₹75,000

Tax payable: 12.5% of ₹75,000 = ₹9,375

Since equity gains aren’t adjusted for inflation, this is a straightforward gain-minus-exemption calculation.

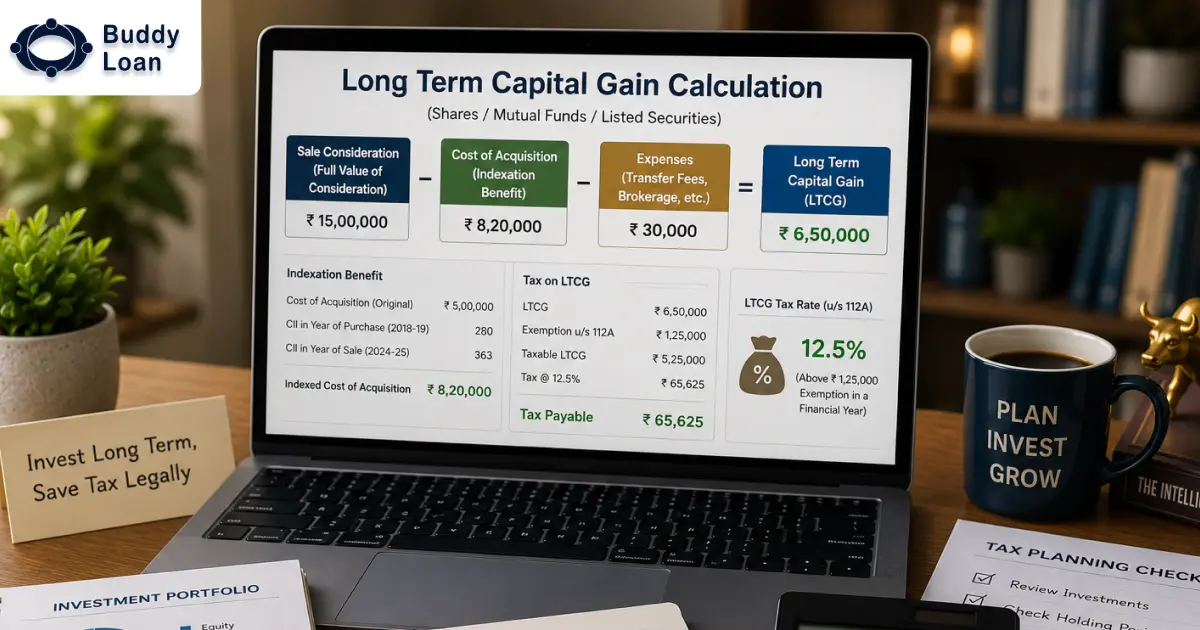

Example 2: Property (With Indexation)

Suppose you bought a residential property in FY 2014-15 for ₹40,00,000 and sold it in FY 2024-25 for ₹95,00,000.

Indexed purchase cost: ₹40,00,000 × (CII of FY 2024-25 ÷ CII of FY 2014-15) = ₹40,00,000 × (363 ÷ 240) = ₹60,50,000

Capital gain (with indexation): ₹95,00,000 − ₹60,50,000 = ₹34,50,000

Tax payable: 20% of ₹34,50,000 = ₹6,90,000

Indexation adjusts your original purchase price for inflation, so you’re taxed only on the “real” gain rather than the inflated rupee gain.

How to File for Long-Term Capital Gains Tax (LTCG)

Filing for long-term capital gains tax is part of your annual tax return. Here’s how to do it correctly as per the IRS 2025 guidelines:

- Use ITR-2 or ITR-3: If you earned long-term capital gains, you need to file either ITR-2 or ITR-3 based on your income type. These forms have a special section where you report your capital gains details.

- Fill Schedule CG: In the Schedule CG section, fill in details like what you sold, when you bought and sold it, how much you earned, and the cost of purchase.

- Use AIS and Form 26AS: Check your Annual Information Statement (AIS) and Form 26AS to see if your broker or mutual fund company has reported your capital gains correctly.

- Pay Advance Tax: If your total tax (including LTCG) exceeds ₹10,000 in a year, you must pay advance tax in quarterly instalments.

- E-Verify the Return: Submit and verify your ITR on the Income Tax e-filing portal within 30 days to complete the process.

Smart Ways To Reduce Long-Term Capital Gains Tax

Reducing your long-term capital gains tax requires careful planning and knowledge of tax-friendly strategies. Here’s what you can do:

- Use Section 54/54F/54EC exemptions wisely: These sections let you save tax if you reinvest your gains in eligible assets like residential property or specified bonds. Make sure to follow the reinvestment timeline and asset type specified by the Income Tax Act.

- Plan sale in different financial years: You can save tax by selling equity assets in portions across financial years. This allows you to take full advantage of the ₹1 lakh LTCG exemption on listed shares and equity mutual funds each year.

- Gift assets to family members in lower tax brackets: You can transfer certain assets to family members who fall in lower or no tax slabs. When they sell the asset, the LTCG may be taxed at a lower rate or even be exempt up to ₹1 lakh in case of equities.

- Use loss harvesting at year-end to offset gains: If you have investments with losses, sell them before the financial year ends to offset gains. This helps reduce your overall capital gains tax liability legally.

- Invest in capital gain bonds under Section 54EC: You can invest your real estate gains in NHAI or REC bonds within 6 months of sale to save tax. These bonds have a 5-year lock-in and a maximum limit of ₹50 lakh per financial year.

- Reinvest in residential property under Section 54 or 54F: If you use your capital gains to buy or build a residential house, you can claim full or partial exemption. The property must be purchased within 2 years or constructed within 3 years of the sale.

Suggested Read: Best Investment Schemes to Save Tax Under Section 80c

Conclusion

Calculating long-term capital gains tax doesn’t have to be overwhelming. If you know how it works and use some smart tips, you can lower your tax and make the most of your investments.

Whether you have been investing for years or just started, knowing how taxes affect your profits is important for growing your money.

Download the Buddy Loan App Now!

One solution to each of your financial needs at your fingertip.

Scan to download now